The Dollar and the Trade Deficit

What will Trump do when his favorite obsession goes the wrong way?

Note: This will be one of my relatively economistic posts. It won’t be nonpolitical — nothing is, these days — but it will be more about narrow economic issues than some.

Sometime in the late fall of 1982 I walked into the office of Martin Feldstein, the chair of Ronald Reagan’s Council of Economic Advisers, and asked whether he realized that the U.S. trade deficit was about to explode to unprecedented levels.

For those who don’t know this, yes, I worked in the Reagan administration. It was a nonpolitical, technocratic position; Marty, an old-fashioned moderate Republican, wanted some of his favorite whiz-kids working for him, and he didn’t care that most of us were Democrats. Here, from the 1983 Economic Report of the President — much of which I wrote — was the Council’s senior staff at the time:

It was an eye-opening experience; my year in government certainly taught me never to assume that senior officials have any idea what they’re talking about. Yet by Trumpian standards the Reagan administration was a model of restraint and discipline. For example, I was in meetings where someone from the U.S. Trade Representative’s Office would point out that a policy being floated would violate our international agreements — and that would be that.

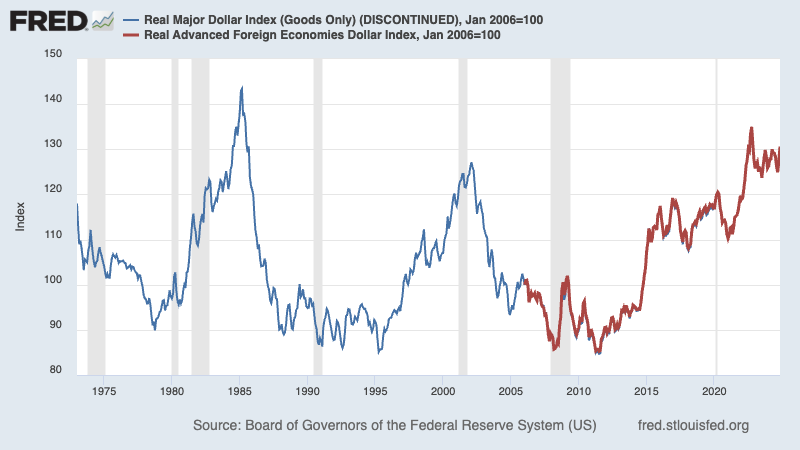

Anyway, the reason I felt safe in predicting a massive surge in the trade deficit was that a strong dollar had already made U.S. manufacturing uncompetitive on world markets. The effect on the trade balance was temporarily masked by the severe recession of 1981-2, which depressed demand for imports. But it was obvious that trade would go deeply into the red once the economy recovered, as indeed it did:

People often forget this aspect of the Reagan economy; the carefully nurtured legend of Morning in America tends either to skip over the big trade deficits or to convey the impression that such deficits were of long standing. In fact, U.S. trade had tended to be roughly balanced until 1980; it was Reagan who introduced our modern era of persistent large budget and trade deficits.

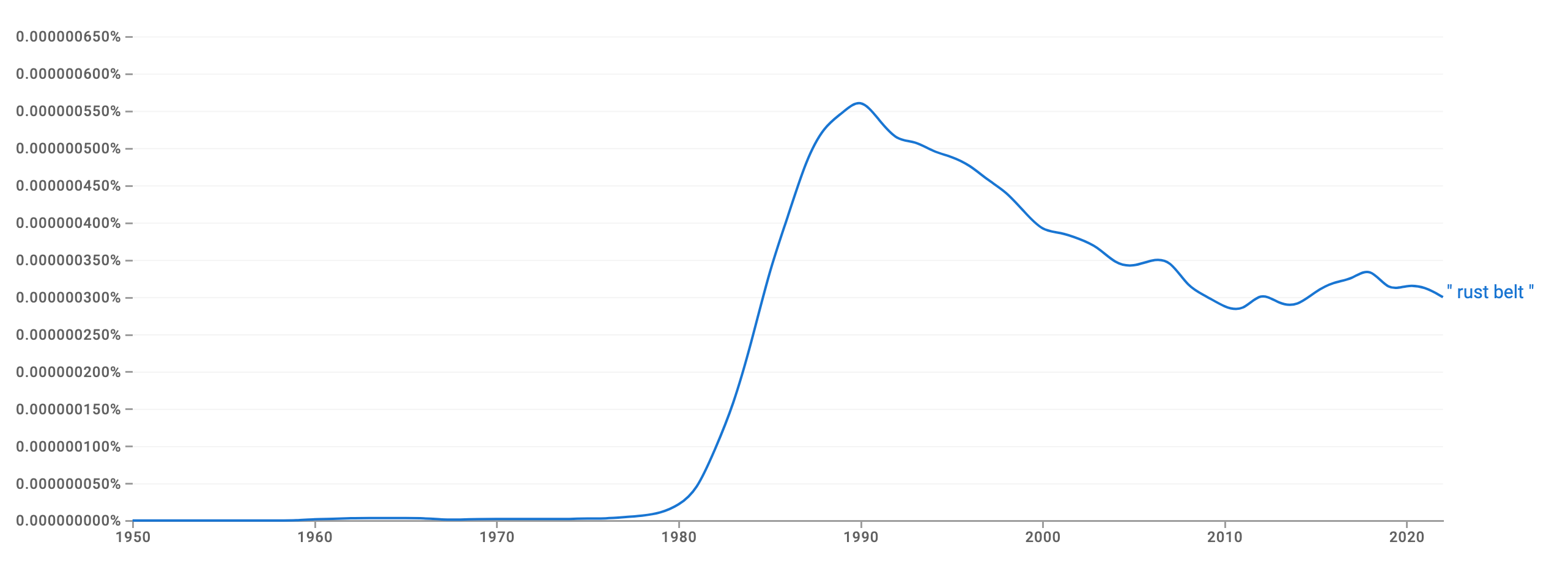

And the trade deficits of the 80s also arguably marked the point at which the hollowing out of U.S. manufacturing really got going. To be honest, it’s hard to find a break in the trend when looking at jobs data, but there was a very distinct break in perceptions: according to Google Ngrams, the Reagan era was when people began referring to the industrial Midwest as the Rust Belt:

So if you’re nostalgic, as Trump and many of his supporters are, for the old days when the U.S. economy was dominated by heavy industry, you should know that it was Reagan, not some bunch of woke environmentalists, who brought that era to an end.

What caused the sudden Reagan-era surge in trade deficits? As macroeconomic stories go, this one is especially clear. (I used to love covering it when I taught undergraduate macro.) By cutting taxes while increasing military spending, Reagan pushed the U.S. budget into deficit. This deficit spending would, other things equal, have been inflationary; but the Federal Reserve contained this inflationary pressure by keeping interest rates high. High interest rates, in turn, attracted inflows of foreign capital, pushing up the value of the dollar.

You can see that soaring dollar in the chart at the top of this post. And the strong dollar made U.S. production uncompetitive, leading to large trade deficits. In fact, for a while the dollar was almost ridiculously strong relative to other advanced-country currencies; in 1985 Harrods, the London department store,

advertised its January sales in the United States, suggesting that Americans slip over to London to stock up on cheap Scottish woolens, cashmere coats and so on. A lot of them did.

But the dollar slid soon afterwards; to this day it remains unclear how much if any of that slide was caused by the Plaza Accord, an agreement by the major economies to try to push the dollar down. In any case both the dollar and the trade deficit declined a lot by 1990.

Then both soared again during the Clinton years. But the story was quite different. Budget deficits were falling, not rising; the driver of Clinton-era trade deficits was a huge boom in private investment, much of it tied to information technology (although during the Bush years the focus turned to real estate.)

Why am I going over this old history? Because there are pretty good reasons to believe that we’re about to see a recapitulation of the Reagan-era rise in the trade deficit.

Trump, after all, clearly wants to make his 2017 tax cuts, much of which were set to expire, permanent; he also threw out a lot of promises of other tax cuts during the campaign, and might try to honor at least some of them.

But, but, Muskaswamy say that they can greatly reduce the deficit by eliminating waste, fraud and abuse. Strange to say, however, almost no independent economists believe them. That DOGE won’t hunt.

It’s less clear whether there will be an equivalent to Reagan’s military buildup. I guess that depends in part on whether Trump invades Greenland, Panama and Canada. It’s also unclear to what extent he’ll go through with plans for mass deportation; if he does, they will cost a lot of money.

We may not be looking at a fiscal shock as big as Reagan’s, but it’s still probably enough to induce the Fed to keep interest rates much higher for longer than most people were expecting a few months ago, which will translate into a stronger dollar and a bigger trade deficit. Also strengthening the dollar: what looks like a spreading economic funk in Europe. And look back at the charts above: we start from both a level of the dollar and a trade deficit comparable to their peaks under Reagan.

But Trump says he’s going to impose high tariffs across the board and punishing tariffs on China. Won’t that reduce the trade deficit? Probably not.

For one thing, I’m genuinely unsure how much taxes on imports will actually rise. It seems quite possible that the coming Trump tariffs will be more about corruption than about protectionism, that many companies both domestic and foreign will in effect be able to buy themselves exemptions.

And to the extent that tariffs do happen, and they aren’t offset by foreign retaliation, they will tend to, guess what, raise the value of the dollar, negating any effect on the trade deficit.

So Trump, who believes that U.S. trade deficits represent a subsidy to other countries — no, that doesn’t make any sense, but so what? — seems likely to find himself presiding over a rising, not falling trade deficit. How will he react?

I guess my concern, shared with many other economists, is that he’ll pressure the Fed to weaken the dollar by cutting interest rates, never mind the risk of inflation. And if he does go down that route, Trump may end up being, among other things, the president who made stagflation great again.

MUSICAL CODA

There’s a real shortage of songs about the balance of payments. But here’s one about inflation, sort of, by a favorite band

Donald Trump doesn’t know any of this. All he knows is that he sees the word “strong” and that must be good.

I know there’s been a concerted effort by our wealthy media class (including your former employer) to get us to forget that Trump is fully addled and was pretty stupid before that, but we’re about to be reminded of that in so many ways.

I did my Undergraduate and graduate studies at UCLA in the 1960s with a big emphasis on micro economics. I then went to work in Corporate America where I worked in corporate staff at a number of the largest corporations in the country. Finally, I ended up as a corporate strategy consultant at PWC where I was chief economist of its strategy practice. So I had an opportunity to observe first hand the transition in corporate management that has taken place over the last 50 years. You mention the Reagan tax cut with out touching on the nature and impact of that cut. The top marginal tax rate from 1917 until Reagan was 70% -95% with the exception of the late 1920s. These high marginal tax rates in effect put a limit on how much money senior executives could remove from the company that they controlled. The tax rates in effect dampened if not completely solved the agency problem. Executives had lots of perks, large corporate staffs, and prided themselves in being the leaders of large commercial empires. In the companies I worked for and the companies I consulted with senior management almost always had life time careers within the company. Executive pensions were closely tied to corporate stock ownership as were many employee pensions (this was pre ERISA). As a result long term growth and corporate strategy was of central importance to the top executives. After the tax cuts when marginal rates dropped to ~35% executives very quickly began to realize that getting as much money out of the company as quickly as possible was the name of the game. In the late 80s and early 90s the hottest consulting projects were head count reduction and off-shoring as well as executive pay advisory.. Short term earnings became the prime focus of the C-suite with strategy being relegated to lower level executives who had an interest in five years out. Executives became hired professionals often with no experience in the industry, but were experts at cost cutting and the shrink to greatness strategy. With the computer revolution of the 90s the tech companies quickly learned that they could sell anything to corporate America if it promised to reduce labor costs,; a strategic objective that is now deeply ingrained in high tech culture. In economics, too much macro focus often often blinds one to the policy impact of changing behavioral incentives. The US has the oligarch dominated, suffering middle class, because that is the outcome that macro policy changes have incentivized.