Hype and Glory

The SpaceX frenzy continues

Source: Bloomberg

Brief post today on amazing things happening in the markets.

While I don’t know anyone who loves Microsoft or its products, it’s a wildly successful company with a long track record. Last year Microsoft earned $125 billion in profits on $318 billion in revenue.

In that same year SpaceX lost $4 billion on $19 billion in revenue. Robin Wigglesworth, editor of the Financial Times blog Alphaville, memorably described Elon Musk’s company as a

very successful but fairly small satellite launch company, bolted onto a stagnant money-losing social media company [X, formerly Twitter] and a money-incinerating AI company [xAI, operator of the widely despised model Grok], and then sprinkled with a lot of hype about humankind going interplanetary.

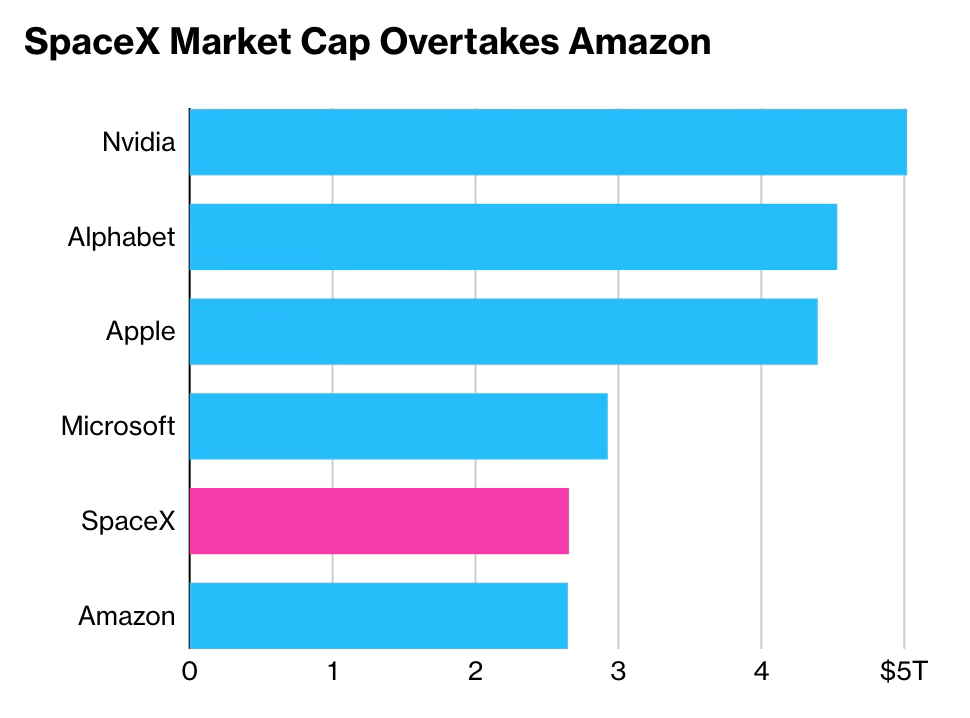

And yet at the end of trading yesterday the stock market placed almost as high a value on SpaceX, which went public last Friday, as it did on Microsoft, and slightly more than it placed on Amazon, which made $78 billion in profits last year.

What can explain this valuation? Many investors appear to believe that Musk is a wizard who can conjure up world-conquering inventions on a regular basis. But while Musk has done some impressive things, his track record for more than a decade has been one of failed venture after failed venture. And his current big ideas, like data centers in space, fundamentally don’t make sense. A recent Government Accountability Office report is carefully worded, but as I read it basically says “this is another Hyperloop [Musk’s absurd, failed attempt to reinvent public transportation].”

Granted, Musk has enormous political influence through his close ties to Donald Trump. So might SpaceX’s valuation be justified, not by Musk’s technological prowess, but by his access to the fruits of crony capitalism?

Nobody should doubt the Trump administration’s willingness to tilt the playing field in favor of its friends, especially those who enrich Trump personally. But there are limits to what even blatant favoritism can deliver.

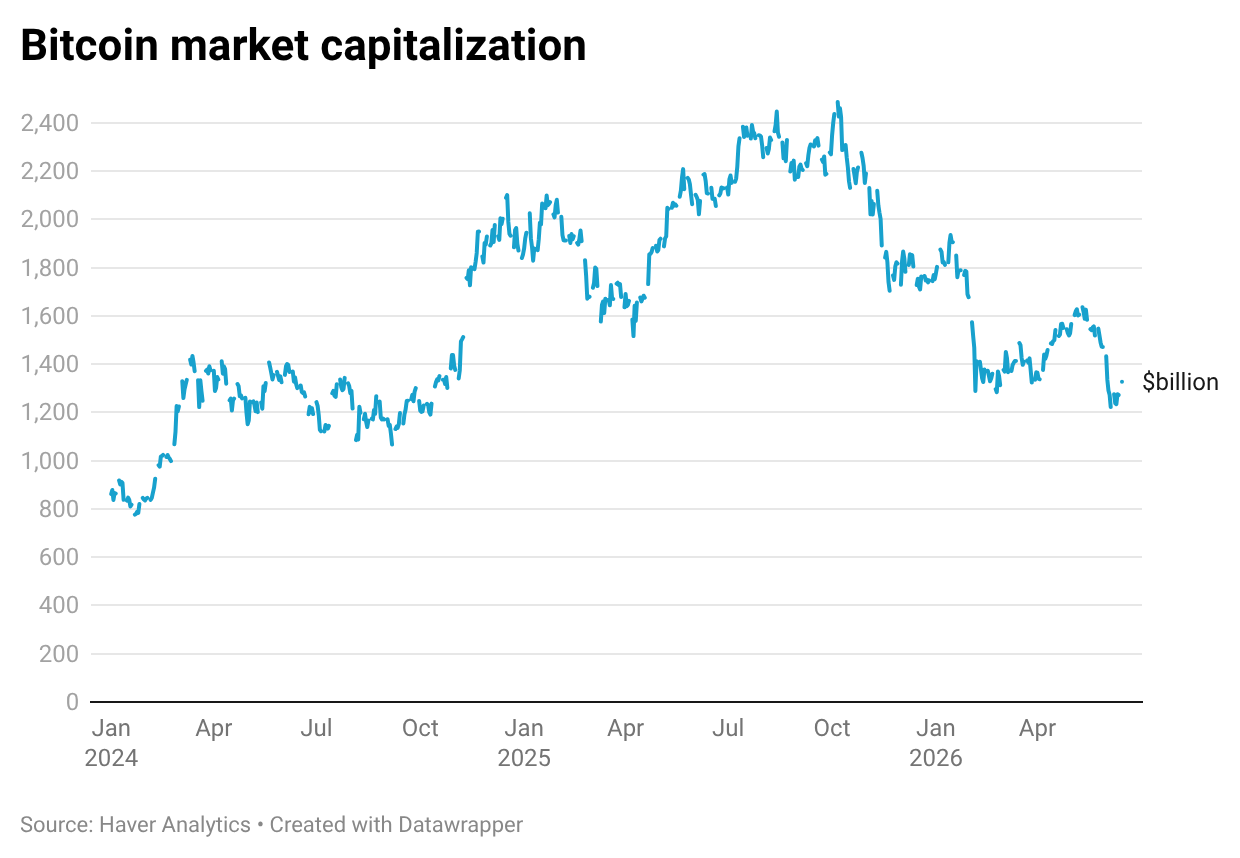

Consider the current fate of the crypto industry. Trump, who once called Bitcoin a “scam,” became a passionate booster of cryptocurrency once it became clear that it was a channel through which he could profit from the presidency. The fighting cage he had erected on the White House lawn was “wrapped in cryptocurrency advertisements.” And cryptocurrency valuations soared after he won in 2024.

But the Trump bump for crypto has now vanished. Here’s the total market capitalization of Bitcoin over the past two and a half years:

At its peak, Bitcoin had a market capitalization similar to that of SpaceX now. Yet the fact that Bitcoin is economically useless for anything other than money-laundering meant that its soaring valuations rested on the belief that the crypto-friendly Trump administration would subvert regulations in its favor, for example by allowing crypto companies to effectively operate as unregulated banks. Hence, as I wrote last year, crypto became a Trump trade, operating under the belief that Donald Trump’s patronage would overcome both economic logic and the opposition of the banking industry and many Democrats in Congress.

Sure enough, as Trump’s poll numbers began to sink, along with his political leverage, so did the value of Bitcoin. But those who got in on the Trump trade early, and sold their holdings to the Trump believers, made big money.

The particulars of SpaceX are different from those of Bitcoin – SpaceX does have one profitable division, Starlink, which was touted as the money-engine behind the SpaceX IPO. Only incredible growth in Starlink can justify SpaceX’s valuation. Yet an analyst who has dug deep into the numbers has shown that the Starlink valuations in the SpaceX IPO imply that Starlink will eventually dominate 80% of the global internet service market. That’s not remotely possible,

So the moral here is that SpaceX is essentially all about hype. It is, in effect, a $2.75 trillion meme stock. The only winners will be those who got in early, stoked a market frenzy, and exit before the bottom inevitably falls out.

MUSICAL CODA

Starlink’s expansion faces growing geopolitical pressure. The global internet service market is not a unified market that a single company can easily swallow. xAI has already fallen behind in the competition. Space-based data centers cannot solve the fundamental problems of radiation and heat dissipation in orbit, and the practical obstacles are substantial: launch costs, maintenance difficulty, thermal management, radiation damage, orbital replacement, data-transmission latency, ground-station bandwidth, insurance costs, space-debris risks, regulation, and militarization.

Over the long run, SpaceX’s space technologies will also face intense competition from China. Its real barriers to entry are not as high as the market narrative suggests.

That is why I strongly agree with the view that SpaceX’s real value is being amplified by the Musk myth, the Trump trade, the AI narrative, the fantasy of space colonization, and index-fund-driven capital flows. On top of a real asset, the market has layered a huge mythological premium.

So Musk has understood that selling hope (belief, illusion) is more profitable than selling cars or rockets. The catholic church has known this for over thousand years.