Health Insurance is a Racket

What value do these companies add, really?

It’s not news that many Americans dislike health insurance companies. In fact, Brian Thompson, the CEO of UnitedHealthcare who was murdered two weeks ago, reportedly warned his colleagues months ago that the industry had a public relations problem. Still, the glee with which substantial numbers of people reacted to his death and the elevation by some of Luigi Mangione, his alleged killer, to folk-hero status has come as a shock.

To say the obvious, murder is bad, and so are murderers. Neither should be celebrated.

But saying that Thompson didn’t deserve his fate shouldn’t require pretending that health insurers play a generally productive role in our society. For the most part, they don’t.

Let me offer a somewhat, but only somewhat, caricatured view of U.S. health care: It’s a system in which taxpayers bear the cost of major medical care, but this taxpayer money flows through private companies that take a cut, spend a lot on administration, and do their best to deny care to people who need it.

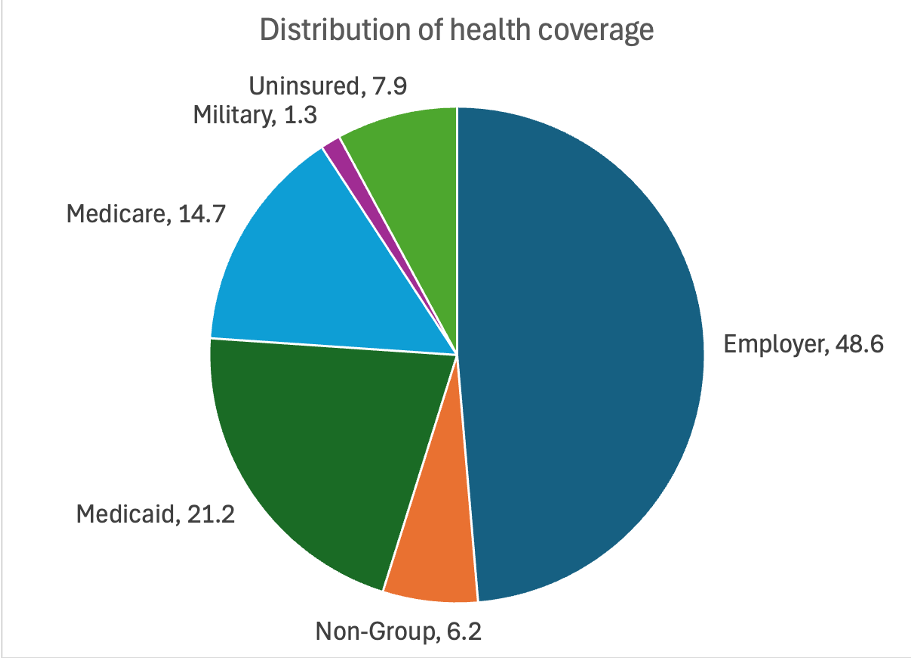

This (almost) reality may not be obvious if you simply look at where people get health insurance. A majority of Americans are covered by private insurers, either via employer-sponsored plans or, a smaller tranche, by individual policies, mostly purchased via Affordable Care Act exchanges:

But medical expenses vary greatly with age, and older Americans are covered by Medicare; many younger Americans with serious health problems are covered by Medicaid. So private insurers pay a surprisingly low share of expenses:

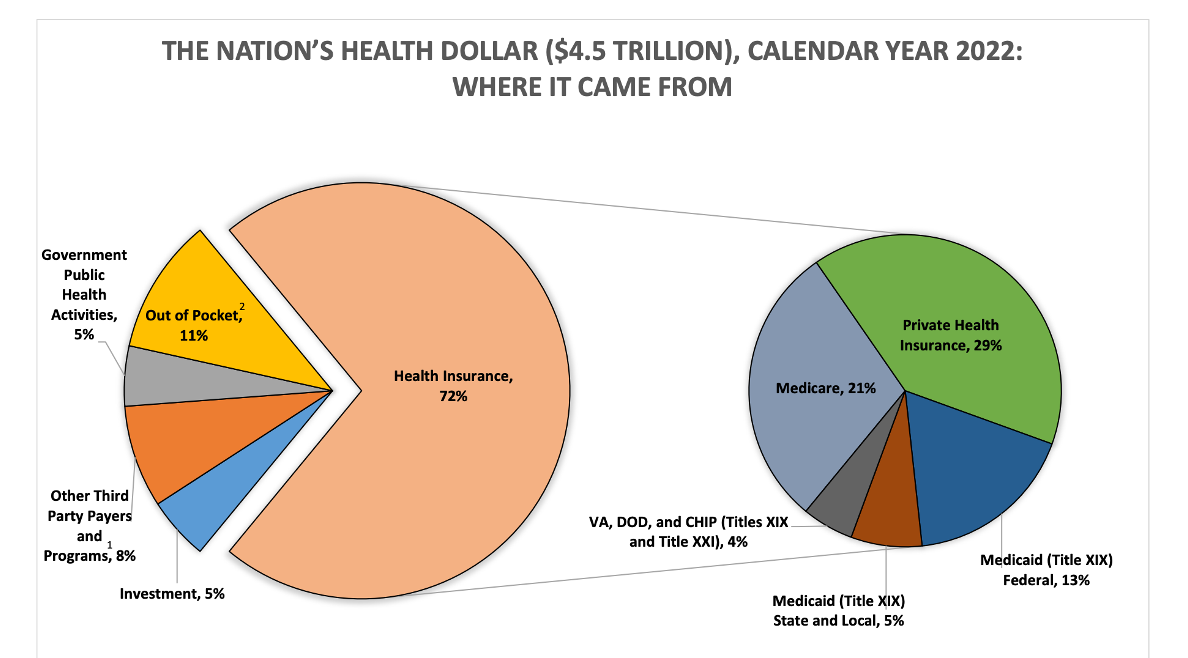

Furthermore, while private companies account for 29 percent of payments by insurers, a significant part of that effectively comes from taxpayers. Premiums on employer-sponsored care are exempt from income and payroll tax, which is a “tax expenditure” — a de facto subsidy — of about $300 billion a year. And most individuals who purchase plans through the Obamacare exchanges receive significant subsidies as well, totaling around $90 billion a year.

So we really have a system in which taxpayers foot the bill for around 80 percent of health insurance. Yet much of that money flows through private insurance companies. In fact, a majority of Medicare recipients now have Medicare Advantage plans, which means that even Medicare passes through the private insurance industry:

In short, I wasn’t exaggerating all that much by saying that we have a system in which taxpayers pay for health care, but the money is paid out through the insurance industry, which skims off a substantial part along the way.

What service do private insurers provide in return for the tolls they in effect collect on a largely taxpayer-financed system? Medicare Advantage plans generally offer more extensive coverage than traditional Medicare. But there doesn’t seem to be any clear evidence that this is because private insurers provide efficiency gains the public sector doesn’t. What happens instead is that Medicare Advantage plans appear to be able to game the system sufficiently that they receive more taxpayer funding per enrollee than traditional Medicare spends on recipients in equivalent health.

Furthermore, Americans who sign up for Medicare Advantage may not realize the extent to which they are exposing themselves to the delay-and-deny strategy private insurers often use to avoid paying for care.

So you could make the case that at this point private health insurance is, in large part, a parasitical racket. At which point at least some readers will ask me why I didn’t back Bernie Sanders in his call for single-payer, Medicare for all.

The answer is that this call was and remains politically unrealistic.

The big problem isn’t the political power of the insurance industry, although that’s nothing to sneeze at (and good luck getting your medical bills fully paid if you catch pneumonia.) The more important problem is that most Americans with employer-sponsored health insurance are happy with their coverage:

True, they’re not as happy as Americans covered by Medicare, and become considerably less happy if and when their health deteriorates and they need to make greater use of their insurance:

But still, anyone proposing a radical reform like Medicare for all is in effect saying to large numbers of voters, “We’re going to take away insurance that you like, that you believe works for you, and replace it with something different. It will be better! Trust us!”

That’s a very difficult pitch to make. In a way, it’s what Bill Clinton tried in 1993 — and he failed badly. If Harry Truman had managed to add health insurance to Social Security in 1947, Americans would take single-payer for granted and be furious if anyone proposed privatizing health insurance. But we are where we are; Obamacare was designed to expand coverage while doing as little as possible to disrupt existing health arrangements — and as some older readers may remember, it barely made it through Congress even so.

So I’m not calling for an attempt to end private health insurance, although if Muskaswamy were serious about cutting government waste, overpayment for Medicare Advantage would be one of DOGE’s prime targets. Also, if wishes were fishes, beggars would ride, or something.

So no, let’s not murder health company executives and lionize their killers. But let’s also not pretend that their industry serves society.

MUSICAL CODA

I agree with Paul Krugman's take here—including his observation that Medicare For All isn't politically viable. But I've long thought that something along the lines of what Pete Buttigieg was touting—more or less single payer for all who want it (aka a public option) would be the best way to get us to where we need to be: robust, truly universal coverage with private health insurance relegated to ancillary services. I believe this concept should be at the heart of the next round of healthcare reform.

My husband and I are 80, and in reasonable.health. We have Medicare and we also have

individual supplemental policies to get nearly full coverage MINUS drugs which, knock on wood, neither of us has had to take very much of. With the SS deductions for medicare and the two "supplemental" policies, we pay $1100 a month for medical insurance. Almost 20% of our gross income. That's real life out here in America.