Why AI Spending Reminds Jim Chanos of the Fracking Bubble

Some of what I learned from the market veteran

Last week I had a video conversation with Jim Chanos, the famous but now retired short-seller. Chanos is a very interesting guy, with an unusually strong sense of history, and of course a very different perspective from those of us who talk about markets but aren’t players. For now, the full interview and transcript are for paid subscribers only. But for today’s post I thought I would intersperse my own thoughts (and confusions) with some key extracts from Jim’s remarks. This is only part of what we talked about, and I’ll do another Chanos-based post soon. For now, however, two topics: Market complacency and the economics of AI.

On the strange complacency of markets

Yesterday I noted that there is a seeming disconnect between, on one side, the economic news (somewhat worrying) and the political news (terrifying) and, on the other, the stock market, which seems untroubled by all of it.

Let me expand a bit on the news that you might think would worry investors. As Employ America has pointed out, “soft” economic data — basically surveys of consumer and business sentiment, which become available much sooner than “hard” data like employment numbers — is showing cracks. It’s not just consumer confidence, which has plunged much earlier than I expected; sentiment among homebuilders and service companies has also fallen off.

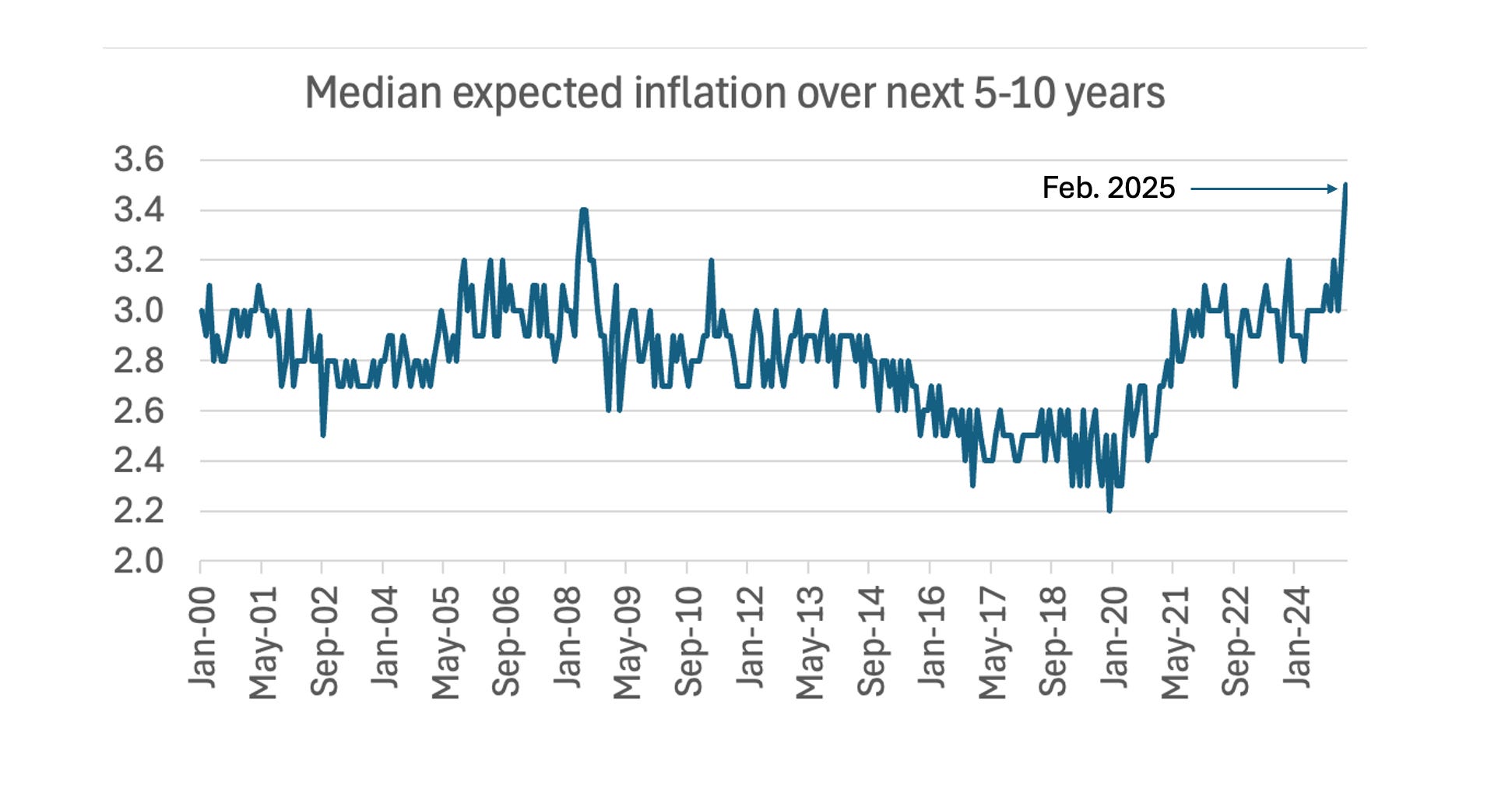

I’ve been especially struck by the fact that medium-term inflation expectations, which stayed subdued all through the post-Covid inflation surge, have now shot up to levels we haven’t seen in decades:

Source: University of Michigan

Meanwhile the federal government is in chaos, with DOGE laying off thousands of employees without making any visible effort to find out whether what they do is important, sending out emails with demands that agency heads are instructing their staff to ignore. Oh, and we appear to be barreling toward a government shutdown in less than three weeks, with little indication that either Trump or Republicans in Congress are paying attention.

Yet the stock market is hanging in there, with investors still buying the dips. What did Chanos have to say about market behavior?

The one thing I've learned after 40 years of running money is that my idea of where the markets are going is pretty much worthless. What you can do at any given time in market cycles is look at things like sentiment and valuation that give you an idea of what kind of risk you're taking. It's not necessarily a timing mechanism, but should anything go right or anything go wrong, what type of risk are you incurring? And right now, I believe pretty strongly that risks are pretty elevated for lots of reasons. We can get into them. But valuations are very, very high. And they're very, very high on what are basically all-time high corporate profit margins, which used to mean revert, but don't apparently do that anymore, as you know better than I do.

And then you've overlaid on this a really, really set of new political economic risks that could really take things in all kinds of different directions with unintended consequences. There's elevated valuations on elevated profitability with a dynamic that is somewhat new in the political sphere.

In short, even if markets seem clearly overvalued, don’t count on them correcting any time soon. But you should always be aware of the risks, which seem exceptionally high right now because of the political craziness — or, as he put it, “wild torpedoes in the waters politically.”

Later in our conversation I brought up one of Chanos’s major successful shorts, the German company Wirecard, which was caught out in fraudulent accounting and collapsed in 2020. What struck me was that Chanos made his bet based on information that was not only public but the subject of extensive reporting:

We did not do the original work on Wirecard. Like a lot of short sellers, we saw a series of reports that had come out of Europe and the UK in 2016 and 2017. So we kept an eye on it. But it wasn't until the FT and Dan McCrum did a series of articles in 2019 that really, for the first time, pointed exactly where the fraud was occurring.in the Gulf States and in the Philippines and possibly Singapore. And then the bombshell for us and the reason we got short in the fall of 2019 in a big way was a follow-up set of articles in the FT with documents. And that was a smoking gun. And what was amazing about that, Paul, was that once you saw the actual documentary evidence, the supervisory board basically resigned a few months later.

They hired a third party auditor to audit the claims of the journalists and the short sellers. And that firm, KPMG, basically said the company wasn't cooperating with them. And the stock still traded for another two months at an insane valuation until the company came out in June of 2020 and admitted the money wasn't there and everything collapsed in three days.

It was a wonderful example of financial cognitive dissonance. From October 2019 to June 2020 you actually had real evidence of fraud and the market still didn't care until the company admitted to it.

“Financial cognitive dissonance.” What I take from that is that markets sometimes refuse to acknowledge what’s right in front of their noses, which seems relevant to our current situation.

AI and the fracking analogy

Another topic we discussed was AI, which has played a huge role in driving up the valuations of a handful of technology companies. When I wrote about it recently, I made comparisons with the internet boom of the late 1990s, built around a technology that produced real economic gains, although not as large as some visionaries predicted. The thing about that boom was that it raised productivity but also cost some investors a lot of money, because they believed wrongly that the trendy companies of the moment would be able to establish long-term, highly profitable market dominance a la Microsoft.

Chanos wasn’t much into that analogy; he thinks this bubble may be worse, and made an analogy I really didn’t see coming:

Forget that. How about the capital being employed? There better be something new. I mean, we're talking now for the just a top handful of companies doing $300 to $500 billion in capex [capital expenditures] annually. I mean, AI isn’t like the internet, which made things more capital efficient and raised returns on capital.

So far, AI is doing the opposite. It is a massively capital-intensive business. Someone joked that the top tech companies are now looking like the oil frackers did in 2014, 2015, where more and more capital is chasing arguably a variable return.

Translation: these days tech companies are spending hundreds of billions of dollars a year on equipment and buildings (the capex he’s talking about), so it’s not like the internet boom, which didn’t involve large-scale spending. And he’s doubtful about whether future returns will justify the current levels of AI spending.

Why did Chanos mention fracking? Fracking is the practice of extracting oil and gas from shale by injecting liquid at high pressure, fracturing the rock. Fracking technology has revived the U.S. oil and gas industries, and along with renewables, has made America energy-independent for the first time in generations. But the fracking companies themselves turned out to be far less profitable than they led investors to believe.

As Bethany McClean, the journalist who broke the story on fraud at Enron, pointed out, the key problem was that “fracked oil wells show a steep decline rate: The amount of oil they produce in the second year is drastically smaller than the amount produced in the first year” — a fact not reflected in their profit statements. (Chanos called it an “accounting scam.”) Chesapeake Energy, one of the leaders in the field, eventually filed for bankruptcy, but not before Aubrey McClendon, its swashbuckling former chief executive, had been forced out. As McClean noted, McClendon died in 2016

when his car slammed into a concrete bridge on Midwest Boulevard in Oklahoma City. He was speeding, wasn’t wearing a seatbelt and didn’t appear to make any effort to avoid the collision.

So how does this relate to AI? Chanos pointed to the huge capital spending that big tech companies are now making on AI:

The numbers are now getting so large from just even a couple years ago that the returns on invested capital are really now beginning to turn down pretty hard for these companies.

…

I've been a bear on the data centers, the old data center companies, because now the new guys are building bigger and better and faster ones and the old ones are obsolete. But the problem is that it's not so much the data centers that depreciate, they do because of the air conditioning and all the guts of them. It's the chips that you're paying $50,000 a piece for that are being leapfrogged by the same company. And so the question is how fast are you depreciating and are we gonna get into the realm of accounting chicanery? How fast are you depreciating these hundreds of billions of dollars if you have to keep re-upping newer and more expensive chips? So, you know, that's where the rubber hits the road and the numbers are getting big enough, that in a couple of years, those are gonna be uncomfortable questions.

Interestingly, yesterday’s news about Microsoft may very well confirm Chanos’ assessment: Microsoft is canceling some leases on data center capacity, possibly indicating that the company believes that it has been securing more AI capacity than it needs. Perchance, did Microsoft listen to my Saturday interview with Chanos?

There’s lots more, for example about the possibly destructive role of smartphones and the parallels between Elon Musk and John Law. But I think that’s enough for today’s post. More in a few days.

MUSICAL CODA

10 out of the last 10 recessions started under Republican Presidents. Just saying.

Interesting comparison to the fracking boom. I would point out that there was also massive capital expenditures for the internet boom — just by different companies. Qwest Communications — and others — installed massive amounts of fiber optic cable, all of which was eventually used — but which led to their bankruptcy when the uptake wasn’t nearly as quick as they had anticipated. The fiber optic cable enabled much of the expansion in data usage through 2010 and beyond — but the companies that installed it had long since gone bankrupt.