Voodoo, MAGA Style

Republicans still believe in magic-based policy

Patriotism is still, I guess, the last refuge of scoundrels. But for the past 45 years or so — ever since Reagan — economic growth has come a close second. The left isn’t completely free from this nonsense, but mostly what we see are right-wing politicians justifying cruel and/or irresponsible policies — massive tax cuts for the rich, harsh treatment of the poor and working class — with the claim that all will be well because these policies will unleash rapid economic growth.

Donald Trump has brought his own brand of nonsense, with claims that tariffs can make foreigners pay for everything. But the old voodoo is still very much part of the mix.

(No, I won’t abandon the term “voodoo economics.” It has a specific, well-known meaning with strong historical associations, and nobody actually believes that it’s an insult to anyone’s religion.)

Which brings me to Scott Bessent, Trump’s pick for Treasury secretary.

The other day I wrote about Trump’s team of economic yes-men, but I didn’t say anything about Bessent, who was widely regarded as a relatively conventional, reassuring pick. Yet Bessent’s “3-3-3” economic plan — or maybe it’s just a concept of a plan, since he has provided no specifics about how he might achieve his goals — is full-on magical thinking.

I won’t talk right now about Bessent’s implausible claims that he can increase oil production by 3 million barrels a day or reduce the budget deficit to 3 percent of G.D.P.; Catherine Rampell is good on these. Instead, let me narrow the focus to his claim that he can raise economic growth to 3 percent.

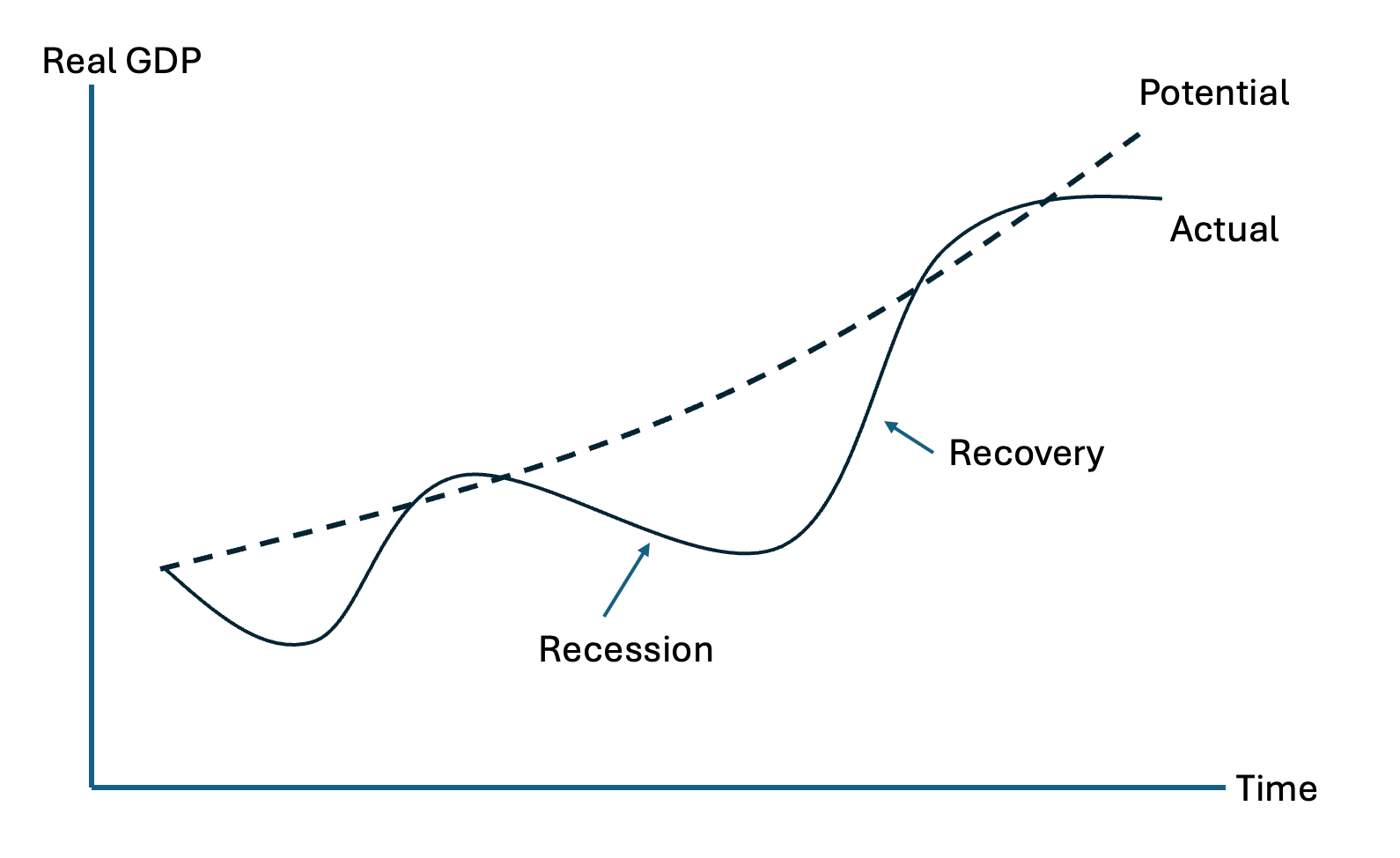

First, what do we mean when we talk about economic growth? It’s always important to distinguish between short-term fluctuations and the long-run trend. Here’s a stylized picture of how the economy behaves over time:

Real G.D.P. has its ups and downs, but these are fluctuations around a long-run upward trend in “potential” G.D.P. — the amount the economy could produce at full employment, or more precisely at sustainable full employment; I show us occasionally going above potential, but these occasions involve economic overheating and the threat of inflation.

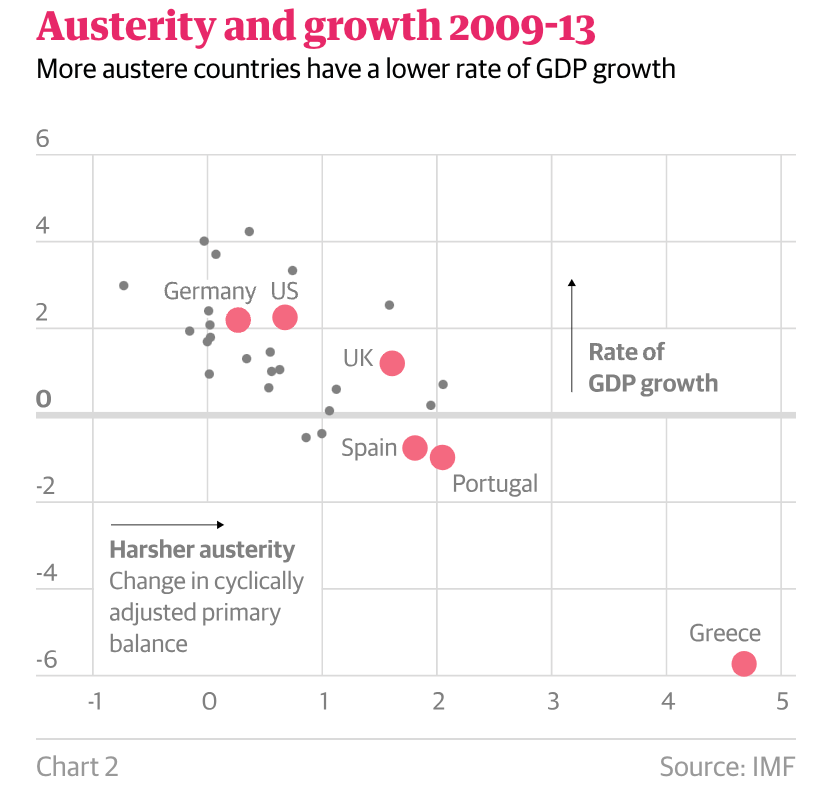

We actually know a lot about how to fight recessions and accelerate recoveries. The clean little secret of macroeconomics is that Keynes was right: expansionary monetary and fiscal policies are expansionary, contractionary policies are contractionary. This becomes obvious whenever we get something like a natural experiment, such as the harsh austerity policies imposed on some but not all European economies during the euro crisis (chart from an old piece of mine in the Guardian):

When someone like Bessent claims that he can raise the growth rate, however, he means steepening that long-run trend. The Congressional Budget Office expects potential G.D.P. to rise about 1.9 percent a year over the next decade; Bessent is claiming that he can raise that to 3 percent. The problem is, nobody knows how to do that.

{kind=link}

Long-run economic growth is the sum of growth in the labor force and growth in productivity, output per worker-hour. (OK, hours per worker can also vary, but never mind.) We could, of course, accelerate growth in the labor force by admitting a lot more immigrants; somehow, however, I doubt that Trump will sign off on that. What about labor productivity?

Well, growth in labor productivity has varied a lot over the years. Here’s a chart from the Bureau of Labor Statistics:

By the way, if you’re wondering about the choice of time periods, the BLS is measuring growth rates between business cycle peaks, applying the Anna Karenina principle: all happy economies are alike, but each unhappy economy is unhappy in its own way. What you can’t see clearly from these data, but we know from closer inspection, is that productivity really took off around 1995, before fading out around a decade later.

Anyway, the question is whether there are plausible policies that could raise productivity enough to get growth up to 3 percent.

Well, Republicans believe, or claim to believe, that they can sharply raise productivity growth by cutting taxes on the rich. You could say that claim is unsupported by evidence. But that’s too weak; in fact, it’s powerfully rejected by the evidence.

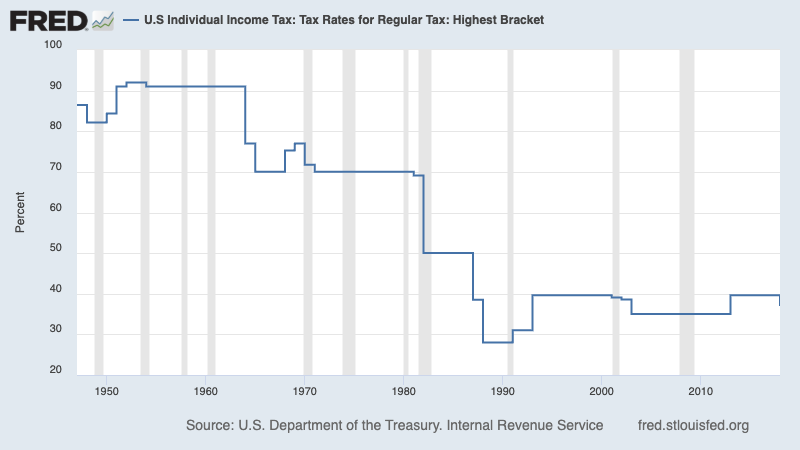

The chart above shows that we had very rapid productivity growth for a generation after World War II. If tax rates at the top play a crucial role in growth, that couldn’t have happened, since top tax rates throughout the postwar boom were incredibly high by current standards:

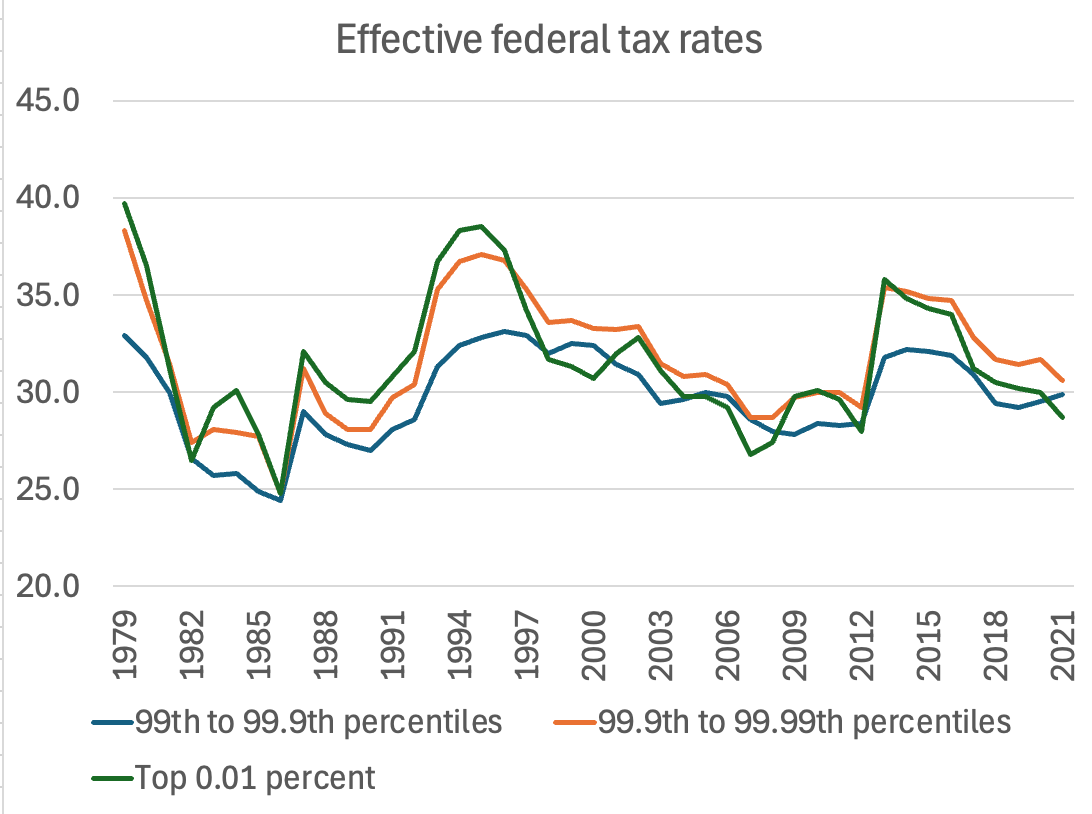

CBO also has estimates since 1979 of the average level of federal taxes on top income groups, which is more informative than just looking at the top tax rate. These show big swings depending on which party was in control:

What’s notable is that the 1995-2005 productivity surge came after Clinton sharply raised taxes on the wealthy, and that a tax bump under Obama didn’t have any visible effect.

I’m not claiming that high taxes on the rich caused high productivity growth. What we’re probably seeing are forces that have nothing to do with policy; that 1995-2005 surge was business finally figuring out what to do with IT. And we could, possibly, see a similar surge in the near future from AI. But there’s no reason to believe that cutting taxes will do anything to boost long-run economic growth.

A personal observation: If you have a high salary and live in New York City, you face a quite high marginal tax rate, because both the state and the city levy income taxes on top of federal taxes. So are affluent New Yorkers slow-moving and lazy because taxes eliminate their incentive to work hard? Not exactly.

Tax cuts, then, won’t deliver high growth. Nor is there any reason to believe that there would be a big payoff to deregulation — especially financial deregulation, which has repeatedly led to disaster.

So should governments just give up on trying to accelerate long-run growth? No, they should do what they can. But they should do so in a spirit of humility, realizing that nobody knows how to make a big positive difference — and shouldn’t base their economic plans on the assumption that their preferred policies will deliver a growth miracle.

I mentioned that hubris about growth isn’t entirely a right-wing vice. I was disappointed that “Kickstart economic growth” was such a prominent part of Britain’s Labour manifesto last year, and that Rachel Reeves, the Chancellor of the Exchequer, continues to put faster growth at the center of her agenda; none of this rises to Republican levels of magical thinking, but I’d be happier with a prime focus on things we know Britain’s government can do, like fix the NHS and repair infrastructure.

I’ll do some posts about Britain once I feel comfortable enough in my understanding of the situation there.

But back to Bessent: markets were reassured by his selection, because he comes across as a normal, sensible Wall Street type. But personal affect is a very bad guide to how policymakers will act. Trump’s future Treasury secretary — I assume he will easily be confirmed — has policy ideas that are, in their own way, as disconnected from reality as Trump’s belief that he can fund the U.S. government entirely with tariffs, at no cost to consumers, or Elon Musk’s belief that there’s $2 trillion a year in wasteful spending hidden under the sofa cushions or something.

MUSICAL CODA

Not Scott Bessent

As the professor said - “You could say that claim is unsupported by evidence. But that’s too weak; in fact, it’s powerfully rejected by the evidence”.

This single statement applies well to ALL the demonstrable lies Republicans believe.

Observations like this one are the reason I love this newsletter: The BLS measures "growth rates between business cycle peaks, applying the Anna Karenina principle: all happy economies are alike, but each unhappy economy is unhappy in its own way."