Stagnation With Chinese Characteristics

How not to manage a downshifting economy

This is a nerdier, wonkier post than usual. Also not about America. Consider yourself warned.

In the early 2000s a small group of New Jersey economists — well, we all worked in New Jersey; you got a problem with that? — formed what Scott Sumner has called the Princeton School. The group included yours truly, Lars Svensson, Michael Woodford and some guy named Ben Bernanke — whatever happened to him? All of us were concerned by Japan’s apparent inability to break out of deflation and worried that Japan-type problems could manifest themselves in other economies, which they did.

Unlike some Western economists, we didn’t think Japanese policy was obviously stupid. We did, however, argue that Japan’s policy response was insufficient and berated Japanese officials for not taking more vigorous action.

But after watching the massively inadequate U.S. and European responses to the 2008 crisis and its aftermath, I began suggesting that all of us go to Tokyo and apologize to the emperor. In retrospect, Japan did a pretty decent job of dealing with a probably unavoidable downshift in its long-run rate of economic growth, avoiding mass unemployment and suffering — which we didn’t.

And China, whose current economic situation bears a clear resemblance to that of Japan in the early 1990s, looks set to do even worse.

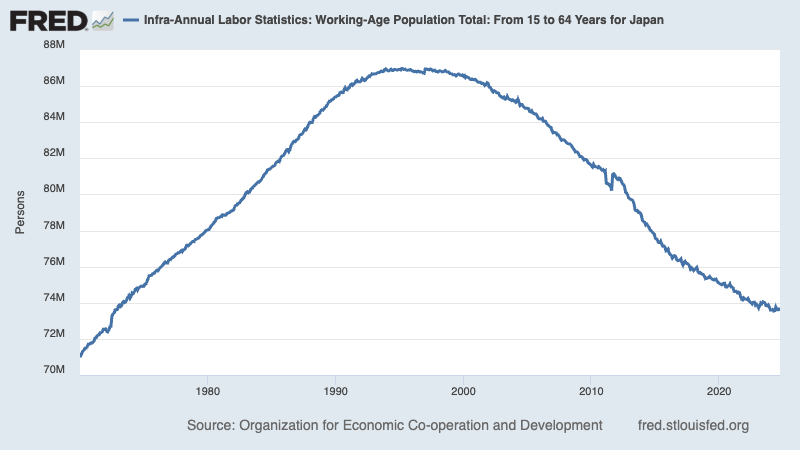

About that downshift: In the 1990s decades of low fertility plus limited immigration finally caught up with Japan’s potential work force; since then the working-age population has been declining at a fairly fast clip:

Note: Yes, I know that people in advanced countries rarely start working at 15, and some of us doddering old codgers keep working into our 70s, but that’s the standard number, and it’s good enough for government work current purposes.

Japanese productivity growth also slowed as the nation came closer to the technological frontier, which meant less ability to achieve rapid progress by borrowing from abroad (such borrowing, by the way, is perfectly fine.) Economists measure technological progress by “total factor productivity,” which is supposed to measure the productivity of all inputs, not just labor; it’s a somewhat flaky number, but still a useful indicator:

Now, a downshift in long-run growth can cause big problems for short-run economic management. An economy with a rapidly growing work force and rapidly rising productivity can accommodate high levels of investment without running into diminishing returns; Japan in 1980 had much higher investment (and lower consumption) as a share of GDP than the U.S. and other Western economies:

I’ll come back to those extraordinary China numbers later.

Without a growing labor force and with productivity slowing, investment at that rate does run into diminishing returns. This can lead to depressed demand and deflation, hence the Japan syndrome. But Japan did reorient its economy over time, supporting demand and employment with deficit spending. And if you adjust Japanese growth by demography, as you should, real GDP per working-age adult has grown at a fairly decent pace:

As I see it, Japan since 1990 is a success story: a nation that experienced a growth downshift for reasons beyond anyone’s control, but managed the transition to lower but still OK growth quite gracefully.

But does anyone expect China, which appears to be experiencing a similar downshift, to respond with comparable grace?

China has now joined Japan in the ranks of nations with declining working-age population:

For what it’s worth, estimates of total factor productivity for China show it flat or declining:

Obviously China isn’t really retrogressing technologically; in fact, it has shown an impressive ability to compete on fairly advanced technologies. What these numbers probably reflect is a combination of massive amounts of wasted investment, especially in real estate, slowing progress in the economy outside sectors the government favors, and a general crackdown on the private sector.

In a way it’s surprising to see such a slowdown in what is, after all, still only a middle-income country; Japan didn’t downshift until it was more or less at the same overall technological level as the West. But China appears to be falling into the middle-income trap — a controversial concept, but one I believe corresponds to something real.

What’s remarkable is that China’s leadership seems completely unwilling to adjust to this changing reality.

As you can see from the chart above on investment shares, China hasn’t moved at all toward the kind of lower investment, higher consumption economy it needs to become. Instead, investment as a share of GDP has gone even higher, thanks to government policies that both fueled a monstrous real estate bubble and pushed investment in government-favored industries even when they already had excess capacity.

A recent report in the Wall Street Journal laid this failure to adjust squarely at the feet of Xi Jinping. Xi clearly distrusts the private sector and wants to strengthen central control; he also has views about consumption — which ultimately has to become the economy’s main support — that sound like a cross between German ordoliberalism and Tea Party conservatism:

Xi views American-style consumption as wasteful, and fears that providing too much state support to households could encourage “welfarism.”

Xi also exhibits an almost Trumpian level of disdain for economic analysis:

As storm clouds gathered over China’s economy earlier this year, a key Communist Party advisory body prepared a report for leaders in Beijing. It warned that China could slip into a deflationary spiral—the kind of disaster that befell the U.S. during the Great Depression—if more urgent steps weren’t taken to rejuvenate growth.

Xi was unperturbed.

“What’s so bad about deflation?” he asked his advisers, according to people close to Beijing’s decision-making. “Don’t people like it when things are cheaper?”

While Xi’s intellectual rigidity is a big problem, however, I also suspect that China’s economic management is being distorted by the country’s sheer size.

For one thing, China may be only middling in terms of per capita income, but it has so many people that it’s an economic superpower — and by all accounts Xi is obsessed with expanding China’s power, economic and otherwise, in ways that would never occur to the leader of a smaller nation.

Also, one way to compensate for weakening investment spending and inadequate consumption is to export your way out — run big trade surpluses. Japan has, in fact, been a consistent surplus nation. But persistent large trade surpluses do cause tensions with one’s trading partners, even if they aren’t run by Donald Trump.

{kind=link}

In Japan’s case these tensions have been manageable because Japan accounts for a relatively small part of the world economy. China, however, is such a huge economy that its trade surpluses loom very large for the rest of the world; the fact that Chinese authorities appear to be playing games with the numbers to make their surpluses look smaller than they really are does not improve the situation.

Now what? China already has high youth unemployment and declining job opportunities. There are growing signs of social unrest, despite the regime’s repression. And I can’t help thinking about the Malvinas scenario, in which a regime whose domestic policies are failing tries to distract the public with military adventures.

What seems clear, in any case, is that the world’s largest economy (by some measures) is on an unsustainable path, yet the person in charge refuses to make a course correction and seems to be in denial about the nature of his nation’s problems.

This seems all too likely to end badly, and China won’t be the only victim if it does.

MUSICAL CODA

Stephen Sondheim explains physiocratic economics

Question. When you relax at your morning coffee, do you entertain yourself by doing high math on paper napkins? You don't have to answer, it's clear that you do, and it's pleasing to know. That your "wonk" is worded for we non-wonks is much appreciated.

Thanks for making these complex ideas so clear. It makes me think about S. Korea, another country that is going through a demographic collapse. I wonder if the recent political upheaval is in someways a response to macroeconomics difficulties that the country faces? All of our allies, Germany, Britain, Italy, Korea, Japan are dealing with a "birth dirth" We are only avoiding it because of our immigration policies which, apparently, are about to be radically worsened.