Notes From All Over, #1

Things to be aware of as Trump Day approaches

So far each of my newsletters has been devoted to a single theme. Going forward, however, I plan on irregular occasions to offer more of a dog’s breakfast collection of items that seem interesting, alarming or (rarely) encouraging.

So let’s start today with news from China, whose government has just announced that the economy grew at a surprisingly strong 5.4% in the fourth quarter. This brings growth for 2024 as a whole to 5%, exactly matching the government’s target.

What a coincidence.

As far as I can tell, most serious China experts aren’t asking themselves why China’s economy grew 5.4%. They are, instead, asking why Chinese officials chose to announce growth at that rate. It’s widely believed, at least among people I talk to, that China routinely overstates its economic growth. Here’s a chart from Rhodium Group, which makes independent estimates of Chinese growth, comparing their numbers with the official numbers (NBS.) If they’re right, China has been overstating its annual growth by 2-4 percentage points:

And the degree of overstatement is a political decision.

However, analysts have to be careful in saying what they really believe about the Chinese economy, especially if they are based in China or do extensive business there. Chinese authorities have explicitly demanded happy talk from economists:

China economists and strategists at leading brokerages say they are hewing closer to the official government line and being cautious in their commentary in response to signs of tighter monitoring.

The latest sign came Friday when the state-run China Securities Journal said the main securities industry body has told brokerages to ensure their chief economists play a positive role in analyzing official policies and boosting investor confidence.

But don’t sneer at the Chinese. It’s entirely plausible that Donald Trump, who has sued the Des Moines Register over an unfavorable poll, will soon be putting pressure on Wall Street economists to say only upbeat things about inflation and growth in America.

All that being said, there may indeed have been a transitory pickup in Chinese growth in late 2024, in part because American firms have been rushing to buy Chinese goods before Trump’s tariffs kick in.

Which brings us to Canada, also on Trump’s economic enemies list.

After an initial, embarrassing groveling visit to Mar-a-Lago by Justin Trudeau, Canadians seem to have found their spine. The Canadian government is reportedly ready to respond immediately with retaliatory tariffs on products including Kentucky bourbon and Florida orange juice if Trump goes through with his threats to impose tariffs on Canadian exports.

My guess is that Trump imagines that because we run a bilateral trade deficit with Canada — they sell more to us than we sell to them — the United States would have the upper hand in any trade war. If so, he’s likely to have a rude awakening.

If you look at the actual composition of U.S.-Canada trade, it suggests if anything that Canada is in a stronger position if trade war breaks out. More than all of that Canadian bilateral surplus comes from U.S. imports of oil and gas:

Outside oil and gas, U.S. producers have more to lose in terms of reduced sales in Canada than Canadian producers have to lose in reduced sales to the United States.

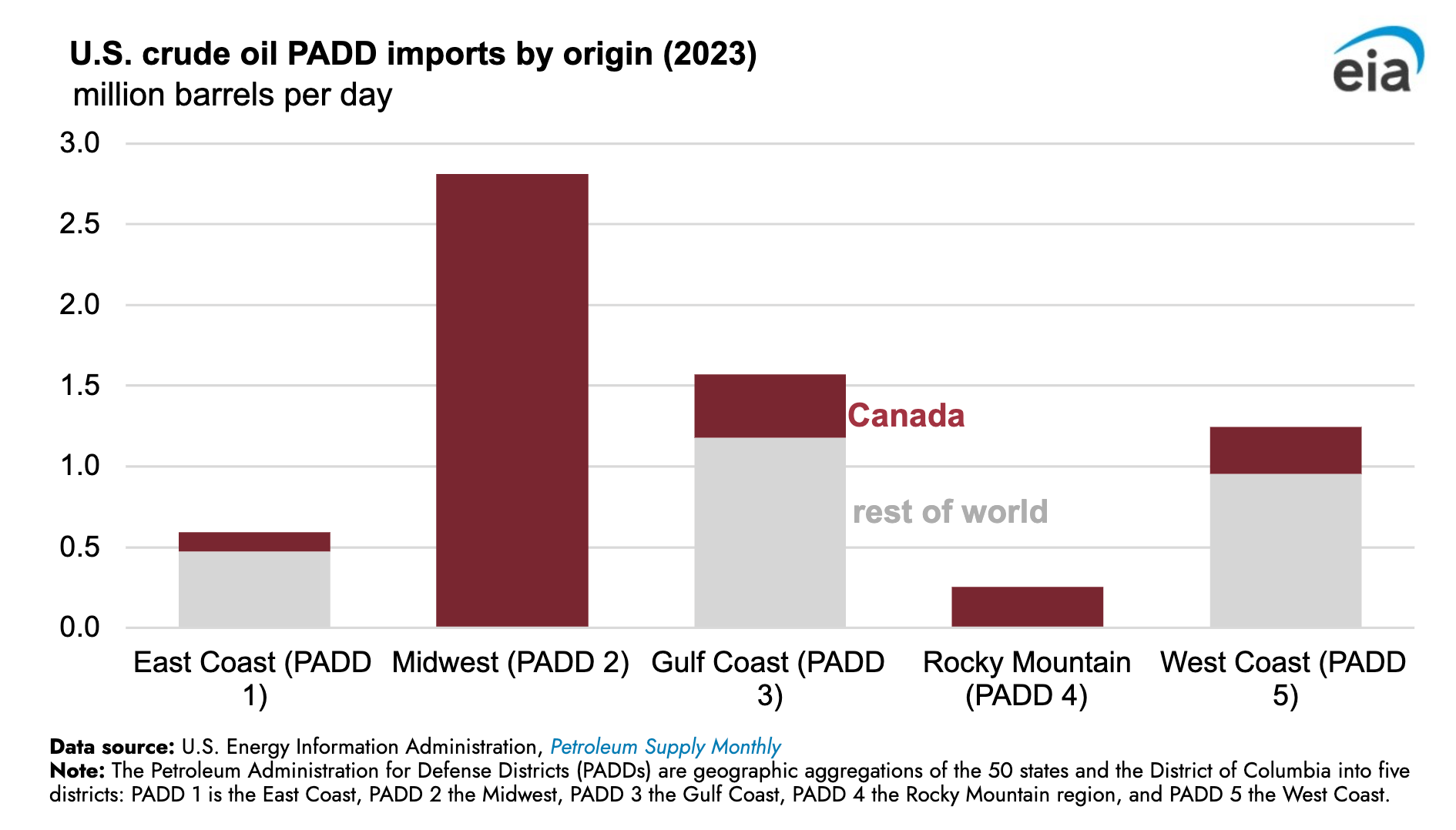

And Trump really, really won’t want to impose tariffs on Canadian oil, which would directly increase energy costs in the U.S. Midwest. The maroon bars show how much each U.S. region depends on Canadian oil, and it wouldn’t be easy for the Midwest to shift to other sources:

Indeed, Canada could weaponize its oil by imposing export taxes, and officials are reportedly considering that option if the trade war escalates.

It’s true that America has by far the bigger economy, which in some sense might give it extra power to punish. Still, a trade war with Canada might develop not necessarily to Trump’s advantage.

Finally, a look across the Atlantic. I’m still doing my homework on the British economy and Labour’s policy approach. When reading other accounts, however, you should know that the British media, on average, do a considerably worse job covering their own economy than their U.S. counterparts, with a special predilection for scare stories about debt and deficits. Simon Wren-Lewis has called this “mediamacro,” and I’d suggest that any journalists writing about economics read what he has to say.

Given this predilection, it was inevitable that the media would be ready to declare an economic crisis even on weak evidence. And to be fair, British economic performance has been disappointing since Labour took office. Still, when interest rates spiked at the beginning of this year, commentators were far too quick to compare Keir Starmer to Liz Truss, who tried to bring voodoo economics to Britain and failed to outlast a head of lettuce.

Funny about that:

This doesn’t mean that all is well. As I said, I’m working on understanding Labour’s policies and the state of Britain, but my assessment certainly won’t be all positive. Clearly, however, the panic was overdone.

And that’s it for today.

MUSICAL CODA

In case you’re wondering, that’s Curt Smith and his daughter.

I don't think Trudeau was grovelling. Canadian premiers wanted him to go. Trump demands grovelling, and no country can afford not to try to ameliorate the situation. The US causes this unprecedented threat to an ally; no need to blame the victim.

Thank you so much…also for the musical codas!!!