Inequality Set Free

And other self-referential stuff

As regular readers know, I’ve developed a routine for the paywall on this Substack. It’s free six days a week, but the long “primers” on Sunday are for paid subscribers only. I’ll talk below about why I do that, but first some news. I’ve just finished up a 7-part series of primers on inequality, and it does seem slightly ironic to charge for those. So what I’m going to do, with a lag, is make that series available free — but not on this platform. Instead, we’ll be reposting entries on the site of the Stone Center on Socio-Economic Inequality, my academic base. Check out the whole site — it’s an incredible resource.

So here are the first two posts in my series:

Why did the rich pull away from the rest?

The importance of worker power

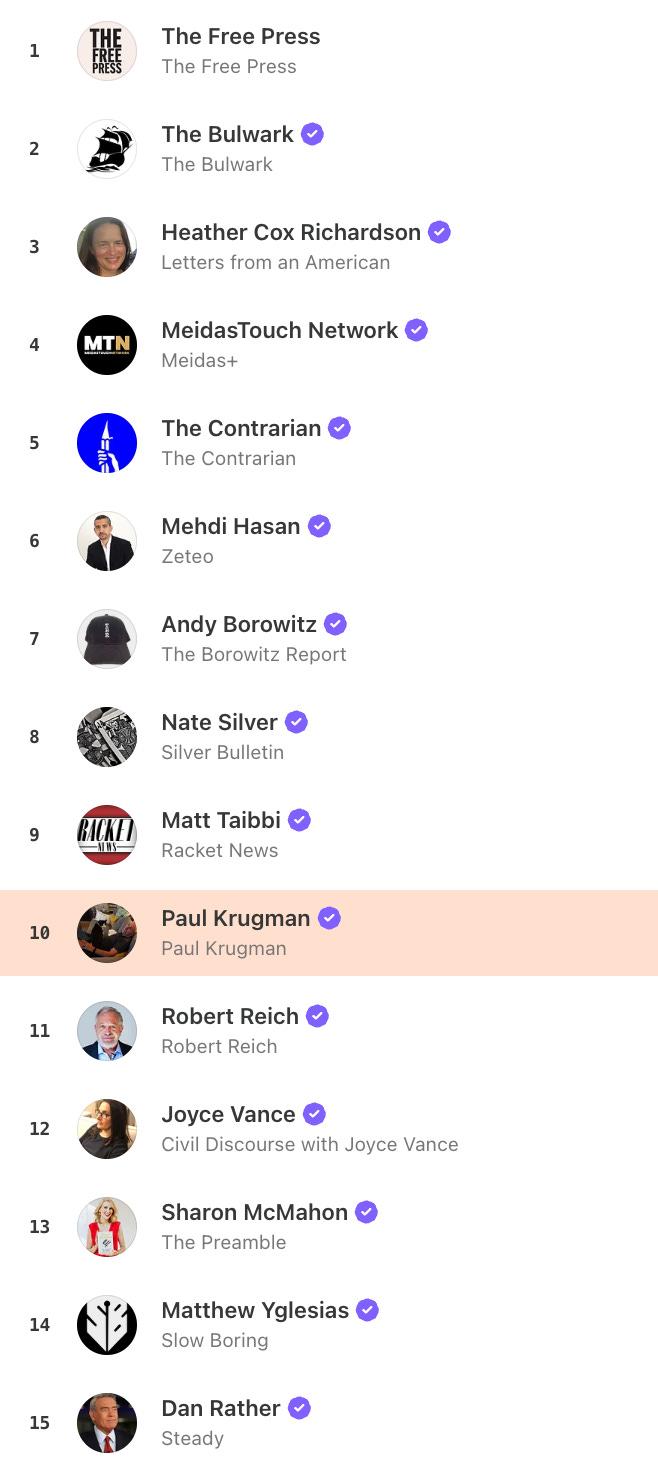

OK, a bit more on the state of the stack. I’m now 7 months into this venture. Its readership and, I hope, influence are still growing, although not at the breakneck pace of the first few months. I recently passed two arbitrary lines I was looking at. Total subscriptions are now over 400K, and I’m in the top 10 U.S. politics bestsellers:

For people telling me that I should quit Substack because it’s a right-wing site, look at the top 10. Two are right-wing; seven are either center-left or Never Trumper; and Nate Silver has a bad word for everyone.

Those bestseller lists are based on paid subscribers, and scoring well on those metrics matters in a variety of ways — which is one reason I’m paywalling the Sunday posts, because those posts are the main driver of paid subscriptions. The other reason is that while money was never my reason for posting here, this has turned into a more than full-time job, in fact a family business — Robin puts in a huge amount of effort on editing and research. So earnings are an incentive to keep on plugging.

Finally, for anyone curious to see me in a more academic setting, last week I was on a panel at the NBER Summer Institute. My segment is below — but don’t click on the embed — it gives you 5 hours of video. Click on “Watch on YouTube.”

Very rough transcript follows.

Incidentally, for those who caught me on MSNBC the other night, they must have MAGA sympathizers on their tech team. As you can see, my face is not bright red:

TRANSCRIPT

Linda Tesar: Hello everyone. My name is Linda Tesar. I'm a professor of economics at the University of Michigan and I'm very pleased to play the role of moderator here for a panel on the global economy.

I think we all are well aware we've enjoyed a long period of stable global relations,

increased trade, increased financial integration. I’ve been involved with lots of papers on those topics. And things have now shifted into reverse. That's the topic of today's conversation: what is the world like now that we have shifted into a different gear and what does the future hold? This is true for trade but beyond trade just relations between countries more generally and what is going to happen to the world going forward.

So I'm thrilled to be here today with two people who need little introduction: Oleg Itskhoki from Harvard University and Paul Krugman of the City University of New York. They're going to start by speaking a bit generally about global financial markets, trade, and where are we going, what's the future, and then I have a few questions I'm going to pose. Then we will open up to conversation and questions from you. Oleg take it away

Oleg Itskhoki: Thanks so much. This is a pretty good turnout for the ITM. There is

this IGM forum on Chicago’s website which is kind of cool. They ask questions to the professors and professors give answers. I thought two pretty good questions would have been nice to ask them before April. One is if US were to go ahead with 10% tariff across the board, do we expect that there is a chance that there is no retaliation from the rest of the world? Is there a chance that the world will just absorb those tariffs and do nothing? And if I were asked, I would have said there is no chance there's going to be a retaliation on a 10% unilateral thing. For the rest of the world, it’s just not an equilibrium for many, many different reasons, right? But now it looks fairly possible

that US might get away if US were to stop at 10% of everybody. It might well just get away with that. I still think it's less likely that it's a loss in equilibrium than not. This is quite surprising.

But then the second question to which I thought I had a very kind of clear answer is: Is it in the interest of the US to have a 10% tariff on the rest of the world with no retaliation? The optimal tariff argument suggests that probably yes. I mean, given elasticities, probably a 10% tariff is a big financial win for the US. If the US can get away with it without retaliation, we should actually advise US policy makers to do that. I've talked with a few colleagues and actually people are skeptical. It's not obvious if this would be the advice that this room would give to the policy makers, that US should go ahead and do that 10% tariff. And just to ensure that nobody retaliates, is it really in the interest of the US? I don't think the elasticities are such that it overshoots the optimal tariff level, but then there are a lot of things we observe in the data that's been happening since April 2. One thing is, it just breaks the structure of equilibrium. We've been in some sort rule-based equilibrium and now we shift into another type of equilibrium.

Who knows how it will look [under a] power-based equilibrium, the loss of allies, and some type of deglobalization? We had a pretty interesting discussion of that yesterday in the panel. The second possibility is, it could be all the stuff that happens in the financial market triggers something. It's not just the tariff per se, but it triggers something in the financial market. The US is at the center of the world financial system because the dollar is the dominant currency. And so, if there's a change in that financial equilibrium, maybe in itself that's a big cost. I'm not sure if I have a comparative advantage to talk about the latter rather than the former. Maybe my comparative advantage is to pass it to Paul right now.

But, I have a few remarks of what has been actually happening in the financial markets. So, with the April 2nd announcement, at first it's not clear what's going to happen at 10% tariffs, but then it's kind of like a 50% tariff or something like that. The stock market goes into a meltdown. What's interesting is, with the bond market, the yields first fall for a couple of days before yields start going up, right? So, yields did not start going up right away. It looks like it's a selloff of both US equities and US bonds and so kind of like the international investors are losing faith in assets.

Then there is a fairly fast mean reversion both in the bond market where the yields came down. With the stock market, if you look at your pension savings, maybe they're not doing that badly from the beginning of the year. But one market which really shifted persistently is the exchange rate. The dollar depreciated by about 10 - 12% against other currencies. It was at a very appreciated level before. [But] if we took a baseline model to think about the effect of the tariff, the baseline model will tell us that when the US does a tariff plan and the response of a currency market to it is a dollar depreciation along the way, the US loses some of its financial position. The purchasing power of US assets that are foreign, when the dollar goes down, it's a net financial transfer to the rest of the world. It's this sort of, like, insurance payment. When the US triggers a trade war and the dollar depreciates, that's like an insurance payment to the rest of the world and that's something we discussed yesterday in the panel, as well. That would be a normal scenario. And in fact, the previous times the US announced tariffs, the dollar tended to appreciate. When Trump was elected, it increased the probability of a trade war and the dollar appreciated on the previous announcement that he did. But [following] April 2, it depreciates and it's the one market that's a very persistent depreciation.

Dominant currencies change about once a century, and the question is: are we lucky enough as researchers to live through an episode like that, and are we actually collecting in data right now how this shift [is occurring] if it ever were to happen? It's actually happening now. And so we actually have some sort of micro data about financial markets where we understand what's going on.

And so, in my mind, if you're a European or Japanese investor for that matter, if you're a pension fund, how confident are you that the financial tool is not going to be used against you if your government is not going to go along. In some dimension, there is some probability it will happen in the future. And so you probably want to shift away from the American assets and we kind of see some evidence in the data that there is that shift from American assets happening but not on a large scale. It's not multiple standard deviation events. These are slow moving things and probably investors are slowly adjusting their portfolios. They now have a target where American assets will be a lower fraction. But it's not enough to just have a desire to sell American assets. You need to have a supply of something else to buy and there is just not that supply out there.

But one market where we see a very clear shift, is the currency market. And so the investors who hold a big exposure to dollar assets, whether it's Treasury bills or corporate bonds and so on, they clearly are starting to buy a lot more insurance. So, in the past, the dollar will appreciate in bad events, and what happened on April 2nd, it massively depreciated. And there is a reason to believe that this is not the only depreciation that happened. As you know, if international investors will be shifting away from US assets, there would be further steps of this depreciation potentially. And so what we see now in the data is that in the futures market, there is a big demand to sell dollars forward. So all those investors that are holding dollar bonds in their portfolio, they cannot quite sell them because there is not that much else to buy. But what they want is the insurance. So they want to sell dollars forward, and when they sell dollars forward, that’s a pressure on the exchange rate and that's what we've been very clearly observing in the financial market. In fact, tomorrow morning I'm going to talk about this mechanism in detail, sort of how it happens in normal times. This is not a normal time but the mechanism seems to have been the same through the kind of futures and forward markets.

What's sort of interesting, and it's a bit of a caveat here, but the covered interest rate parities didn't move. Exchange rates moved a lot but the covered interest rate parities didn't move. They stayed fairly stable. So it was not like a financial crisis when typically the CIP shoots up, right? It was really like a big shift away from thinking of the dollar as a safe currency. Not yet a shift from seeing treasury bills as a safe asset, yet, but from the dollar as a safe currency that appreciates in bad times. And people now want that insurance and the result of that insurance is that the dollar is weaker.

There are all sorts of interesting consequences of a weaker dollar for the trade balance, for sort of general rebalancing and so on. But what's interesting is it’s kind of the first step along the ladder of losing dominant currency status. Perhaps it’s a possibility to say that this is just a blip in the data and a few quarters out it would not be that important. But this shift is very interesting.

Another question is whether there is really exorbitant privilege for US borrowing? Right now when when you look at the CIP data, say against Japan, the CIP itself did move. But what's remarkable is that there is a 4% annual interest rate difference between the US cost of borrowing on US debt and the Japanese cost of borrowing on Japanese debt. So it's not like the US has any privilege in the cost of borrowing. And indeed, you can sort of see it in the fiscal capacity of the US. And I think this is a huge open question for the next year perhaps.

Linda Tesar: Thank you. Before I pass the mic onto Paul, I already failed as moderator. I was supposed to say as a reminder that the NBER promotes economic research, including the economic evaluation of the effects of public policies. But we are not making policy recommendations today.

Paul Krugman: I actually did read that advisory and I'm actually sick of making policy recommendations. Nobody ever listens anyway. I'm also a little sick of big thinking about the future of the world economy because I don't know what the world economy is going to look like on August 2nd, never mind beyond that. So I thought I would just talk about two things that I’m somewhat puzzled about that seem relevant here. One of them is when and why did trade agreements stop mattering, and the second is how should we be thinking about the distributional effects of tariffs. So, two quite different questions.

With trade agreements, I don't know what the mix of trade people versus macro people is here but we have, or had, an international system that was very much based upon international trade agreements. We got to this relatively open world economy through 90 years of trade agreements beginning with the 1934 Reciprocal Trade Agreements Act. It’s always been negotiated agreements. And for some reason, it wasn't until like this morning that I asked, why are these agreements and not treaties? And it turns out that it's more procedural than anything else. A treaty is passed by the Senate with a two-thirds vote. An agreement is passed by both houses with majorities. It's not at all clear that an agreement is any less serious than a treaty.

So, it's a contract. And we built the relatively open world economy—until the other day— on a system of binding international agreements which were taken very seriously. I mean, a lot of people here are way too young to remember, but when NAFTA was being negotiated, tariffs were already pretty low pre-NAFTA, but the idea was that by having a formal agreement you would add a certain permanence, and it was deeply controversial. It was an extremely hard political goal.

So, okay. Yesterday, we began getting a bunch of trade letters posted on Truth Social. Uh, it's a different world. And by the way, be sure they're genuine. Someone did post a perfect mockup that looked exactly like the other letters, except this one was to the Heard and McDonald Islands, which are inhabited only by penguins. But anyway, it started with South Korea and Japan. Now, the United States has a free trade agreement with Korea. We do not have a free trade agreement with Japan, but Japan has most favored nation status, which means that US tariffs on Japan are bound. According to international trade law, we do not have the right to raise tariffs on Japan above what they were set at in the last set of trade negotiations, which I guess is the Uruguay round, so it's passed. We have what we thought were binding contracts, binding legal agreements that say that we cannot just go ahead and raise tariffs. And what did the letters coming from the White House say about why we are breaking these agreements? Nothing. They didn't even mention them. And as far as I know, most media coverage hasn't even mentioned them. I mean, there’s tons of stuff about South Korea but no mention at all in anything that I've read except in economist Substacks, of course, and yet that was a big deal and a very hard set of negotiations. It was actually hard to get it through the legislators in both countries. The Koreans and our congresses had to have their arms twisted hard. And so, all of a sudden it just doesn't matter. And I don't actually know how that happened.

For what it's worth, I spent a year in government long, long ago in the Reagan administration, though subpolitical. People don't know I was senior international economist at the council, alongside senior domestic economist Larry Summers, whatever happened to him.

Anyway, but you would sit in on inter agency meetings, and in the Reagan administration, if the guy from USTR said of some idea being floated, “Look, that would be GATT-illegal,” end of story. We had made an agreement and the United States honored its agreements. So how did this happen? How did we lose that? It’s not just Trump. Why doesn't anybody seem to care?

And by the way, this is kind of on Oleg's point about a 10% across the board tariff. And not to think about it in terms of trade but maybe what it does to the whole system. The principle that agreements are agreements and you don't break them, lightly at any rate. So I don't actually quite understand but that's my first puzzle.

Secondly, a lot of people imagine that economists think free trade is wonderful, that it's great for everybody. That's not at all what “textbook international trade theory” says. Stolper Samson is kind of the origin of 20th century trade theory. It said that very large distributional effects can cause declines in real wages if you reduce tariffs on labor intensive imports. So there was a period quite some time ago now when we worried a lot about the general equilibrium distributional effects of globalization. There were huge arguments about to what extent could rising US wage inequality be attributed to globalization. Should we be thinking about all of that stuff now? How should we be thinking about the distributional effects? And I have an answer. But I'd be curious what other people think.

I think not because there's a funny thing about all of the income distribution effects of trade literature, which is that it all depends on incomplete specialization. Protectionism can raise real wages if it leads to an expansion of labor intensive industries. But if you're just out of those industries entirely, then it doesn't matter. Then a tariff is just a tax. It's just indirect taxation. And you can argue that the way you would have analyzed the distributional effects of tariffs 25 years ago, 30 years ago would be very different from the way you would want to analyze it now. So there was a time when you could actually talk about whether the highest tariff rates that were announced yesterday seemed to be on countries that export a lot of apparel and we're really going after Bangladesh and all of that. And this might seem good for the US apparel industry, except there is no US apparel industry, right? There’s basically nobody. There are a few high-end items, but there's nothing. Near my office, there's a statute three times life size of a garment worker huddled over a sewing machine because it is the garment district, but there are no garment workers. And even with these tariffs, there is not going to be a US apparel industry. So it's not hard to see that any of the kind of labor intensive industries that might matter for distribution are affected at the margin.

What you're left with then is that we have a set of indirect taxes that are essentially a sales tax. I was looking to see if there's anything you can take out of what gets hit and apparel does get hit especially hard. And I thought, well, that should be regressive on top, except, as far as I can tell, apparel as a share of consumer spending is surprisingly flat across the income distribution. I think it may be that the higher top quintile spends less on stuff made in Bangladesh than the bottom quintile but that's not obvious from the data.

But there's a further argument and I'm probably talking too long but let me just say that people have been arguing that this is especially regressive because people at the lower end of the income distribution spend a much higher share of their income than people at the higher end. And so it's an extremely regressive tax and rather… You kind of know what my attitudes are here, which I guess I'm not allowed to say, this being the NBER, but I'm actually nervous about that argument because I think Milton Friedman had a point. Yes there's a very strong correlation between income and the savings rate at a point in time. We also know that there's no trend in the savings rate over time. And the way to explain that is to say that a lot of what you see is in effect a statistical illusion.

If you look at the bottom quintile of households, it's going to be a lot of people having an unusually bad year. If you look at the top quintile, it's going to be a lot of people having an unusually good year. And it's not clear that the share of spending out of permanent income, whatever your definition of that is, is all that strongly related to income level. So, it's not clear to me that the tariffs are as regressive as they might appear. I've been trying to get some clarity on that. But of course what we're doing is certainly a large indirect tax which is, at best, slightly regressive and it's being used in part to pay for reductions in income taxes and income taxes are definitely progressive. So the combination is regressive but there's a lot that I don't understand yet. I don't think there's any case that these tariffs are progressive because they might be if we still had the industries if we had any chance of actually expanding the industries that are being tariffed but I think we're not.

But anyway, those are the two questions I have. And the big thing about what the hell is happening to the world, god knows. Maybe we don't have to answer that in one go here.

Linda Tesar: So, you touched on many things but let me follow up one of them, and come back to something Oleg talked about which is financial markets and the reaction. We recently had a jobs report that looked good. The inflation numbers look good. We even had today announcements of tariffs on copper and potentially on pharmaceuticals. And we write a lot of papers about trade policy uncertainty that even if we don't impose the tariffs, supposedly all of this uncertainty must be very bad for investment and the economy. And we've got this forward-looking stock market that seems to be going meh. So is that 10% is just fine and that's where we think we're going to settle? Is it really that the gains from trade aren't so very large so this isn't going to be all that harmful? How do we make sense of this?

Oleg Itskhoki: So I have a very quick remark on this. It might well be that two quarters from now it's all just a blip. So there is April 2025 and then there is an aftermath which lasts a couple of months but from the perspective of financial markets and even currency markets, it might look just like a blip and we're back to business unusual, with the dollar in the status of a dominant currency and so on. But so far, it looks like we did not have a financial event in April. So the measures of premium didn't go up. The stock market recovered fairly fast. So it doesn't look like it's been a financial event of that sort.

The one market which looks different is the US dollar market. But why there? To

discuss that there is a massive shift in equilibrium and a type of equilibrium that we live. But why doesn't it look like much from the perspective of the financial market? It's hard to say. I mean you can take a perspective of sort of inelastic financial markets here. There is a lot of wealth in the world. The wealth was not diminished in the world economy. That wealth needs to be allocated. At first it might have seemed like the wealth will be shifted out of equities and put into bonds and then you take it out of US bonds to put somewhere else, in bonds elsewhere. But there is not that much assets and so that wealth still needs to be allocated and so far investors decided that they're pretty happy with the portfolios that they have.

And this is the reason why we didn't have a big financial episode. But I mean this is just kind of a guess of what's going on.

Paul Krugman: Yeah, assuming that the markets know something is generally dubious. I'm a big devotee of the old Paul Samuelson remark about how the stock market had predicted nine of the last five recessions. I don't think there's any reason to believe that the markets are representing some kind of sophisticated view about how all of this is going to turn out, particularly the stock market which has a lot of retail investors who are not doing much analysis. I mean, the interest rates are up a little and the dollar is down substantially. That's a completely unprecedented correlation for the United States. That's an emerging market sort of thing. Although it's a sort of order of magnitude smaller, right? It's sort of like Brazil divided by 10 is what we're seeing in that divergence.

But I don't know how much you want to read into it. Economists in general tend to over state how important trade is in terms of gains. Not that it's tiny but it's one of those things where I think there are a couple of factors that lead people to overrate the importance of trade. One is that it sounds important, right? “Global” always sounds important. It's like the international role of the dollar. The amount of obsession about it relative to what we think it actually does. And the other reason economists love to talk about trade is because comparative advantage is something we understand and the barbarians don't. So, I'm looking a lot at the PIIE stuff. You know, the losses from protectionism, trying to keep up with it. But there we're talking 1-2% of GDP. We're not talking about massive changes from where we are now.

I think it might be worse than that for a variety of reasons.

Linda Tesar: But so let me turn it around then. I think from the US perspective that might be so. But of course it might be very, very important to other countries. And so the question is, using our policy of non-policy advising but policy analysis, how should countries respond? Should they be working collectively through the WTO? Should they be unilaterally negotiating? Should there be retaliatory tariffs? Should there be trigger strategies in their responses?

Paul Krugman: I mean, there's a huge difference between economic superpowers and the rest. Roughly speaking, within the limits of measurement of comparably sized economic powers in the world, it's the US, China and the EU. And the Chinese are actually taking it arguably very tough. They're holding back rare earths and batteries. That's actually a lot more damaging, as some might say, in terms of that kind of confrontation, it's a lot easier to offset lost export jobs with Keynesian stimulus than it is to conjure new industries into existence. And so if there's a full-time conflict between the US and China, the Chinese would appear to be in a stronger position.

The EU is being cautious, but the EU is always cautious. I think the Trump people have said there will not be a letter to the EU. It's interesting that there are these really quite harsh letters to Japan and South Korea but no letter to the EU. And where we actually know that people in the Trump administration really dislike the European Europe in a lot of ways. So why isn't Europe getting the same treatment right now? And part of the answer might be that the Europeans are big enough that [the White House] might be a little bit worried about what happens if the Europeans strike back.

So I will predict what I think eventually happens is that we do see a lot of kind of trade arrangements made that just bypass the United States. I mean, Canada is talking pretty openly about trying to switch to a European focus although geography is not on their side.

Linda Tesar: Right. Right. So as you know we're very well integrated with other countries, both in financial markets but also trade through the fragmentation of production and production occurring all over the world. Is there a way that the world goes forward with the US outside of the trading arrangement and these global value chains persist but with Europe becoming the hub and we're just on the outside of that relationship? Is that a world?

Paul Krugman: I think it's not clear. I haven't actually tried to do the arithmetic on it, but I think if Europe and China (and Japan and then Australia) but if Europe and China can maintain more or less amicable trading relationships, I don't really see why you can't continue to have… I mean, I don't think the value chains that include European and Chinese products make much of a stop in the United States along the way as it is. So, sure. A WTO minus one that kind of drops out the United States does look feasible.

Oleg Itskhoki: So, it seems in terms of fragmentation of global value chains for goods that could be perfectly fragmented and target different markets. But the other important area is services. And where US was sort of an undisputed leader is in financial services and payment systems and so on. So I think a huge question is: are we going to see a world where there would be parallel payment systems? That's a world that we haven't lived in. Or will US still be providing the financial and payment system services to the world?

And Paul made the analogy with developing countries. You can make an analogy with Brexit. Another good analogy of April 2nd is how the US started looking like UK after Brexit and it's the loss of the status of the financial center in the case of the UK. In the case for US, it's the possibility that there's just going to be parallel payment systems and US is not going to control it. And that's when we're talking about the dominance of the dollar and the dominant status of the dollar. That is the goods market. Where the euro was a very successful project is a lot of trade has shifted to being denominated in euros, right? Where euro has not been a very successful project isn't necessarily bringing down yields on borrowing in Europe. And this might well happen now.

And the other thing is there is no alternative payment systems. All payment systems go through dollars right now. But I think the big question going forward is: is it going to be the case that we're going to see a fragmentation in the financial system?

Paul Krugman: Yeah, we have no idea. And, you know financial types get apocalyptic about what happens if we disrupt our current financial system. But why wouldn't they? I mean, that's kind of their thing. There clearly would be higher transaction costs if we went to a system where you were largely doing payments in euros rather than in dollars. But these are very small costs. So it doesn't look infeasible. People will probably just be really reluctant to do it, right?

Linda Tesar: Oleg, you made an analogy to a ladder, and have we taken the first step on the ladder? I mean, after Bretton Woods broke down, it's not like it's a switch where you immediately flip over to a new way of doing business. We could fumble around for a while, I think.

Oleg Itskhoki: Well, in fact, it was very interesting. The role of the dollar increased after the end of Bretton Woods because like a lot of de facto pegs to the dollar, the euro became de facto. But then what's amazing is the ascent of China since 2005 actually reinforced the role of the dollar because China was very crucial for the dollar based financial system. It was using the dollar to peg to it, it was using the dollar for savings, to denominate what’s trading. But now we we might actually see the effect of China becoming a big player and actually wanting to create a lot of these parallel systems.

Paul Krugman: China has a [confidence] problem, however. We're worried about the US not honoring agreements and China certainly has a reputation as a place where, you know, they have capital controls, so it has a reputation as a place where a contract is a suggestion. That kind of inhibits the potential role for renminbi. So, if something else

steps in, I would think more likely it would be the euro but it's really hard to move.

I mean I think maybe my favorite paper in all of economics was the old article by Charlie Kindleberger about the international role of the dollar and the international role of English as being essentially parallel. It's really, everybody speaks English because everybody speaks English and it's really hard to move off that. And the dollar may be almost equally hard.

Linda Tesar: Well, I'm aware that I'm in a room with many experts and I've had the chance to ask questions that I wanted to ask, but I should open up the floor a bit if anyone would like to, just ask.

Audience question: So, thinking about the sort of post-war period and formation of the GATT. So the GATT was a sort of international rules-based system.. You think about it as a way of escaping that we're a nash equilibrium and you know moving towards the efficiency frontier and if you bargain according to non-discrimination or reciprocity

countries are symmetric you get all the way to the efficiency frontier otherwise you get some way towards the efficiency frontier not necessarily all the way but that bargain was based on a sort of set of expectations throughout the world and maybe now the world is different the sort of China has opened up policies changed in a different way and so now the world economy looks different and so maybe that initial bargain and that

point that we negotiated to initially might not be the optimal point. And so one sort of way you could interpret some of the recent changes within a framework of economics would be an attempt to bargain to a different point. So to move away from a rules-based system to a more power-based bargaining system and presumably to move to a different point towards the efficiency frontier because the problem that creates also creates a lot of uncertainty. But on the one hand maybe you can renegotiate and move to a different point and there could be some gain from that. But on the other hand, as Paul mentioned, you've destroyed agreements. You've created uncertainty and that might be particularly costly in a world of certain cost. So I wonder whether the sort of panelists had any kind of thoughts about that general challenge of in a world of uncertainty where unexpected things happen and you might want to renegotiate agreements, how should we think about that? We don't really have a a way of thinking about it in a lot of our kind of models of trade policy.

Paul Krugman: So, first, the case for reciprocal trade agreements. I do take the

Staiger Bagwell stuff seriously but fundamentally I do believe that the purpose of all of this stuff is is to protect us from ourselves; that trade agreements are fundamentally a way of disciplining our own special interests. And I don't see any way in which the world has changed that invalidates that point. I mean, there was this problem of accommodating China and that flipped, but I think what’s relevant is, if we think that there is some strategic thinking going on that is driving what's happening, who exactly do you think is doing that strategic thinking? I mean, we know who the players are in the current US administration. We know how trade policy is being made. We know how the April 2nd tariffs became the quite different April 9th tariffs which was that the Secretary of Commerce and the Secretary of the Treasury managed to get into the Oval Office and talk the president into completely changing his tariff policy while Peter Navaro was in another meeting. That doesn't sound to me like there's some grand strategic vision under play here.

So I think the way we set up trade policy in the United States is kind of unique in the amount of executive branch discretion which was given. It wasn't stupid. It was that we have all of these restraints that come out of international agreements but it was

clear that you needed some kind of pressure release valves so the system couldn't be too rigid. So we gave a lot of discretionary power to the executive branch to put

tariffs on various grounds in the expectation that the president of the United States would have a bigger view, a more global view of things than the US Congress would.

Which worked really well for a long time but now you have a situation where pretty

uniquely you can have radical policy changes with no legislation. A lot of this is just trying to model the mind of one man.

Oleg Itskhoki: I have just two quick remarks on this. So, I think it's just absolutely fascinating to think about the nature of equilibrium we used to live in before April 2 and the nature of the new equilibrium. We sort of all know how the Nash looks

like. Nash has fairly high tariffs. That's maybe something like the world was before the great depression or after the great depression and before GATS and WTO. We

don't know how after the second world war we got to what was there in that system, which was strategic in that the US provided coordination by punishing everybody else. But who provided discipline for the United States? Was it the cold war and the need to have aliens that provided what was the nature of the equilibrium? That was robustly played for decades until it broke.

But another interesting thing, it's not just April 2nd. I think what’s quite remarkable is the way TPP died. And I'm in a room where people know a lot more about this than I do, but TPP died from both parties. Neither party wanted to own TPP, right? Both party candidates wanted to kill it. If you think you're now in a new world, it's a new cold war and you're trying to isolate China and build aliens out of China, not through WTO, but TPP was the perfect way of doing it. But neither party wanted to go ahead with that. And that was clearly another structural break in, 2016 or 17 that happened. And how do you

make sense of that over here? If the euro is going to start taking some of the role that the dollar has taken in the past, do you expect Europe to need to generate trade deficits, fiscal deficits, and do you see a willingness in Europe to do some of that?

Paul Krugman: There’s a mostly false belief that the US must run current account deficits to supply reserves. There are other kinds of capital flow. I think Brad Setser recently did that and over the past 10 years essentially none of the US current account deficit has been financed by reserve acquisition. The US current account deficit reflects a lot of private purchases of bonds, of equities from direct investment. There’s just too many margins to operate on. So the United States is not obliged to run deficits even if the dollar retains its role. It's just not how this thing works. I think there are lots of things to worry about there, but I don't think that's one of them.

Oleg Itskhoki: I think if you're a pension fund in Europe or in Japan for that matter, you really are trying to think, if you will not be holding the US treasuries now or US corporate bonds, what else can you put in your portfolio, right? And so I think it's just kind of fascinating that in order to actually have a safe asset, you not only need a demand of it, you need a supply of it, right? And in a situation when there is no supply of bundes bonds or no supply of other kinds of equally safe assets, they cannot rise to the level of the safe asset status, right?

And so, after what happened in April, there is an opening for an alternative safe asset

provider. Europe has a plan to have a lot of expenditure. Well, Germany does. A

lot of Europe cannot do it because they're at the peak of their fiscal capacity anyways and that's a problem. But potentially in some scenarios of the simulation that we live in, this is the opening for another safe asset provider to come on stage. Looking at the data so far, we don't see that happening. But this is a slow adjustment. The investors will decide if they probably want to diversify away from the dollar assets and that process can take a long time. Are we going to see an emergence of alternative asset classes that will take that role? I think that's a big open question.

Linda Tesar: I mean I don't want to suggest I'm a market insider or anything, but to the extent I have had conversations with investment bankers, they're talking about this. They're, like, actively on the table. They're thinking about how to diversify their portfolios

and how to manage this because they're reading the tea leaves and thinking total

dependence on the dollar could be a big mistake.

Oleg Itskhoki: Absolutely. Especially if you're like European pension fund, then you don't want to be in that position.

Linda Tesar: Well, this was JP Morgan.

Question from the audience: Just to keep on this international role of the dollar theme and Paul, you know, you said that people are obsessed with this relative to what it actually does, and we were just having a conversation about the safe asset

side. I mean, if there were to be a substantial decline in the international roles of the dollar, where do you think the consequences would show up? Which functions of the dollar, were they to change, would have the greatest consequences? We know that the dollar is used heavily in price setting on trade transactions on financial transactions. It's a portfolio um issue as you were just saying on safe asset side and insurance. So what are the concrete changes that would be the most impactful?

Paul Krugman Yeah, I would say financial and trade transactions both it's treasury bills as collateral. It's kind of you know it's oversimplifying but largely we the the that T bills have been the universally accepted collateral and lots of transactions are enabled by that and if people don't trust now we're talking you know it's short-term US assets not not not 10-year bonds but if you actually thought that the the Steven Miran white paper was a guide to administration thinking, which I don't, but if if it if you did, it it does talk about attempts to force foreigners not to use our stuff. And it's not clear to me that you couldn't be using uh three-month German Treasury bills for for a lot of this particularly if the Europeans get any anywhere closer to some kind of eurobond you know restoring the integration of their bond markets. I don't think you could do it with Renminbi because I don't think you would be sure that that you would always be able to get your money out if it was actually in China. And how important is it that we have a really really easy to use form of collateral? Aren't people more creative? You may remember that there were a lot of talk that that Russia was going to implode when they were shut out of the Swift system. and they certainly paid a price for it, but you know, they're still still in business. So, I I think that's we probably overstate how important this is. We take infinitesimal transaction costs and raise them to twice infinitesimal. How bad a thing is that?

I mean it's it's odd to answer to Linda on this because she knows better than I do perhaps but the way I think about it safe asset could be replaced by another safe asset but how and it's really like how would the change in the payment system happen now to go across currencies you have to go through the dollar right like dollar is really yeah the interbank market the payment system the settlement you have to go between any two currencies through the dollar right like I just in my head I'm not sure how that change will happen but to me that's the the biggest perhaps change changing on an asset and like investors coordinating on some other asset seems a much more feasible thing but how actually the payment structure and funding structural change to me that's the most robust actually role of the dollar right now sudden worldwide demand for people who still know COBOL.

Also, we've just completely abandoned a whole host of agreements between sovereign countries almost without comment and add to Mark Carney's point where he said Canada will now have to go forward no longer assuming good actions by the United States are no longer really counting on it. I'm curious if you think this spreads and is this really just a trade issue or you know does it extend to you

know defense procurement AI social media like how much of the global economy starts to shift radically if we are in a world where people just no longer assume the US is trustworthy.

Paul That's immense. It's a completely different world I mean probably the book that I read most recently that had the biggest impact on me was Farrell and Newman onweaponized interdependence and they do kind of sort of say what if people start to think that the US will abuse its position and that's no longer hypothetical and economics is in many ways the least of it.

Question from audience I think some kind of consensus has emerged that in pre world one under the first administration Trump the Americans had to eat up muchof the price and pieces from the I wonder what's your view on this time around if something structural has changed and maybe the foreign exporters will eat most of the price or if we are in for a repeat where the Americans have to eat it?

Paul To eat 25% tariffs foreigners would have to cut their prices by 20% to offset that How many producers out there in the world do you think have 20% margins?. I mean if it was 5% tariffs maybe but 25%.

Question from audience This is more a question for Oleg. So you talk about the payment systems having to go into the US dollar. Uh how does the emergence of digital currencies affect that?

Oleg So one of the uh tools certainly being used by different foreign governments but in particular the Chinese Chinese government is digital currency. They are angling for

that uh spot as a reserve currency. So there's sort of push and pull factors. There's the push away from the dollar from within the United States. And by the way, Iunderstand that some policy makers actually want a depreciated dollar. Um, and then there's also the pull from a month basis. So just wondering how that affects us. Right now it's not a competitor in terms of market share yet, right? Like if we predict five years out, uh, obviously any type of turbulence of the kind that we observe in now increases the probability of a shift, right? But like if you just extrapolate out of today, those shares are just tiny, right? It's still a conventional payment system that goes through the dollars. Uh can we be uh confident that that's how it's going to stay? Right? The more sanctions are used, the more financial sanctions are used, uh the more trade policy isunpredictable, it all increases the probability of a shift, right? But if I were to evaluate the probability of that shift in the next five years, I would still think of it as low. But I'm a theorist, right? So I guess this is something that uh really much more applied empirical people should answer.

Question from audience So we're living world now legitimacy of institutions being challenged and I think we all agree that US action is an existential challenge WTO. So as a professional economist um and this is the question to both of you would you defend the legitimacy of the WTO and if so on what basis as an economist?

Paul I think that the GATT still makes perfect sense. It was actually funny is you know we need reciprocity was the line on April 2nd but the whole system is based on reciprocity.

Under the WTO the the ground rules are essentially the GATT; the WTO just adds, mostly, other people may dispute but I would say mainly the dispute settlement mechanism. GATT cases dragged on forever and WTO you got decisions much sooner but at at no point has the WTO itself had any real power. That's true of institutions in general, right? Institutions are people and uh um they have power to the extent that people have agreed to abide by them. And as of certainly like 2016, we had a system in which the the United States and the European Union who were the big upholders of the system granted the WTO a lot of power and would abide by WTO decisions even if they went against them. Um, and I don't think that's a problem with legitimacy. Maybe can we have a WTO with the United States effectively on the sidelines? Uh you know, it's it's certainly not logically impossible. I don't see that there's a crisis of legitimacy. I think that the crisis is that one of the major players has just decided that we don't care.

Oleg I think and I think also Bob your points yesterday were sort of exactly on this. It's we've been in a rule-based equilibrium somehow. What supported that equilibrium I think is a big question and I think it was the goodwill or commitment on behalf of the big player that supported that equilibrium. There was nothing else that was supporting it. Why the calculations has changed right we in different simulation of the world there could have been two big players right like you know 15 years ago one could have imagine a grand bargain between US and China that this would will be the two big players that support perhaps a different rule-based system but clearly now on an equilibrium path we see that there is no rule-based system and uh this is probably costly for everybody involved but supporting the rule base requires a commitment on behalf of somebody. I think it's super interesting what gives that commitment power.

Paul Well, we can have a long discussions. 10 years ago, I thought we had a rules based system based on dual hegemony by the United States and the EU.

Yeah. And the EU I think is would still be willing to do that.

Oleg No, that's the amazing thing. So like if somebody and I'm far from being an expert in this room obviously, but if somebody asked me before April 2nd, what

would be the scenario to respond to the US? I I thought countries will take the template of WTO of response and EU would act together perhaps together with the UK and maybe even with Canada but it's clearly not what's happening right so EU is not leveraging their power in the system at all right they're not responding because you think that was the simplest template to say let's do what WTO tells us to do in response to violation of the rules but that's just not happening no but this is happening but this is happening everywhere right like you the cooperative institution falls apart the legal institution doesn't hold and then it's the unilateral bargaining sets in so that you can get your side down. This is this is what tariff space lets you do it. It creates room for uh wink wink nod nod I'll give you a special arrangement and then but you don't want to act alone right you have the biggest bargaining power when you act collectively and EU has this benefit of collectively but they it's also true that you know in some ways it's early days yet as we'll say.

Paul You know a lot of people uh a lot of people in the markets believe you know taco Trump always trick us out a lot of people believe that that all of thiswill just sort of go away uh at the end of the of this. I think I think they're foolish, but I think the EU is kind of reluctant to get into a full-on trade war because they're hoping that I mean I think probably the formula I think I'm I'm still steer and clear of policy advocacy, but I think the formula that many countries still have in mind that the EU has in mind is to offer some meaningless concessions that can be spun as a great victory for the current administration and then it all goes away.

Linda I think on that note uh we will wrap this up. I want to thank both of you. continue our conversation over Mexican uh enchiladas and tacos. And uh you brought up taco. I did bring up tacos. That that would be definitely the thing to do. Go have tacos.

Glad you made the move from the Times, and very happy to have your more free wheeling views shared so widely.

For the record, I pay NOT for the behind paywall stuff (no reflection on quality) but because I want to help people get free access to your views.

More people can read your views here for free than could at the Times.

Keep up the great work.

FYI, I pay because your Substack posts are ones I always read and I think your work is critical at this moment in time. Thanks.