Cooling it on overheating

Explaining to myself why I'm not worried

As recent economic controversies go, the debate over whether the Democratic rescue plan is too big is like a vacation in Cancun, I mean Camelot — a break from the zombie wars that dominate most policy argument. Compare it with the “debate” over whether wind power caused the Texas blackout!

This time there are sensible, well-informed people on both sides — Olivier Blanchard, who’s worried about overheating, is almost pathologically reasonable and open-minded (in case you’re wondering, Olivier, that’s an admiring compliment), and I always take Larry Summers seriously even when we disagree. But the economists at Goldman Sachs (no link), who aren’t worried about overheating, aren’t exactly irresponsible big spenders; neither are Gita Gopinath, the IMF’s chief economist, or Janet Yellen.

However, the controversy is also pretty much moot in terms of actual policy, at least for now. As a practical matter, Democrats have little alternative to going through with something very close to the full $1.9 trillion. Their proposals are wildly popular; failure to deliver on those $1400 checks would be seen by many voters as a betrayal of promises. And let’s face it, when the opposing party is an enemy of democracy, there’s an extra reason to do what’s popular.

So this plan is not going to be drastically scaled back on the word of technocrats, especially when the technocrats don’t agree among each other.

Yet economic analysis should be done even when it won’t matter for policy in the short run; among other things, those of us in this game should lay down markers that can be tested against what actually happens. And I personally am feeling that there’s an itch I need to scratch; why, exactly, do I disagree with smart people like Olivier and Larry? Lots of people are doing similar exercises, and I make no claim that mine is necessarily better. This is mainly about explaining, not least to myself, where I’m coming from.

So what I want to do here is a bit of numerology. That is, I’ll offer guesstimates on the numbers surrounding the rescue package, in the full awareness that these numbers will be off one way or the other. As best I can tell, my numerology looks a lot like Goldman’s, or the IMF’s. At the end, I’ll talk about what happens when (not if) reality differs from the projections.

The first step is to ask where we are right now.

Minding the gap

Here’s the four-quarter rate of growth of the US economy since 1980. Two episodes stand out: the Morning in America surge coming out of the early 80s slump, and the 2020 pandemic plunge:

We’ve partially bounced back since the summer; real GDP in the fourth quarter was only 2.5% below a year earlier. However, that number is worse than it looks, since between growth in the working-age population and productivity improvements we normally expect the economy to grow around 2% a year. So we’re roughly 4.5% below trend.

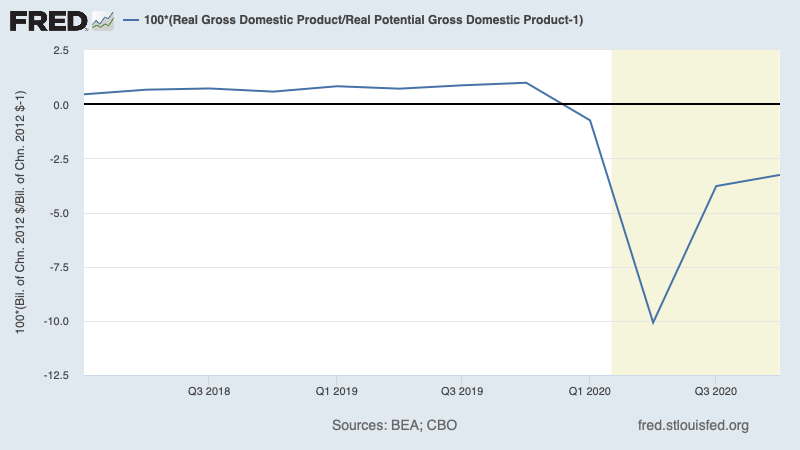

Or maybe not. CBO estimates a Q4 output gap under 3.5%; Goldman, on the other hand, puts the gap at around 6%. What accounts for the difference?

The main answer involves what you think about the state of the economy pre-pandemic. CBO thinks it was somewhat overheated, running about 1% above potential output:

But it’s hard to see why. Inflation was subdued, below the Fed’s 2 percent target. True, the U3 unemployment rate was low; but other measures, like the prime-age employment rate, didn’t suggest a red-hot economy. Here’s a scatterplot of prime-age employment versus core inflation since 2000:

This suggests that the 2019 economy actually had a bit of slack — say 1%. If so, that implies that we were down 5.5% at the end of 2020; as I said, Goldman puts it at 6%.

Morning in America II

Just about everyone seriously engaged in this debate, myself included, expects the U.S. economy to come roaring out of the gate as the pandemic subsides and the relief money goes out. As an aside, I wonder how Republicans will react if, as most of us expect, Joe Biden gets to preside over an economic boom comparable to Reagan’s Morning in America (and a boom for which he deserves more credit than Reagan ever did.) There may be some serious popcorn shortages!

But will the boom push us into dangerous inflation territory? Short-term forecasting is a black art, which even the gurus don’t do very well (and I am not a guru, at least on this.) But let me offer two approaches, both of which suggest to me a boom that gets us close to full employment but not deep into overheating.

First, let’s take the Morning in America comparison seriously. Peak Reagan-era growth was about 8% over a year. True, the fiscal stimulus behind that growth was much smaller than we’re about to experience, but there was also a huge drop in interest rates, which won’t happen since we’re already at the zero lower bound. Also, demography was different then, with the working-age population growing ~2% a year vs. 0.5% now.

So a MiA boom now would mean something like 7-8% growth Q4-Q4. But gap closing would be smaller, because the economy has trend growth around 2%. So we’re looking at a gap reduction of 5-6% — i.e., roughly enough to close the gap and restore full employment, but not to lead to major overheating.

An alternative route would compare projected output gaps with and without stimulus. (No, the American Rescue Plan isn’t intended to be stimulus, but it will nonetheless have a stimulative effect.)

Even without the ARP, the economy would probably grow substantially this year. CBO says a bit less than 4%. Again, however, this would only close the gap by ~2% by the end of the year. And if we’re trying to assess stimulus, we want to know not the situation at year-end but the average over the year, roughly half that much. So if we use a revised estimate of the late 2020 output gap, absent the ARP we’d have a 2021 gap of around 4.5%.

The bill is, of course, considerably bigger than this — around 8% of GDP (although it will come in cheaper if unemployment drops rapidly, and with it UI payments. Also, rapid growth will lead to less spending of aid to state and local governments.) My view, however, is that the rescue plan will have a relatively low multiplier: a lot of those $1400 checks will be saved or used to pay down debts, a lot of state and local aid will be banked in rainy day funds.

The IMF appears to agree, estimating a GDP boost of 5-6% spread over three years.

We still might be talking about a fiscal stimulus bigger than the output gap, but not all that much bigger.

And bear in mind that all these calculations assume no tightening by the Fed. Maybe I missed this in my macroeconomics classes, but it seems to me that fiscal policy should not be aimed at producing exactly full employment at a zero interest rate. You want it to go beyond that, at least a bit, so that the Fed has some room to respond when, as the bumper stickers don’t exactly say, stuff happens.

Which brings me to the balance of risks.

Asymmetry, revisited

We are not now in a conventional recession; output is depressed, but it’s not a normal output gap. But if the relief package falls short we could have a conventionally depressed economy, operating below capacity with interest rates at the zero lower bound, by late this year. And we don’t want to be there! That was the big lesson post-2009: if fiscal stimulus falls short and monetary policy lacks traction, you’re in big trouble, because you can’t count on being able to pass another stimulus.

On the other hand, if the relief package turns out to be significantly bigger than needed, the Fed will have to raise rates somewhat to avoid major overheating. And this will be a terrible thing because … why, exactly?

True, bond markets might experience something of a shock, something like what happened in 1994 — a shock that burned some investors, but did nothing to derail a very solid real economic recovery:

So even though the pandemic economic crisis is very different from the financial crisis of 2008, the asymmetry of fiscal risks remains. Fiscal policy that falls short can be a catastrophe; fiscal policy that overshoots is, at worst, a nuisance.

So hey, big spenders: don’t let the wonks (by which, of course, I mean the other wonks, not me) make you cautious.

Thank you for doing this substack with some depth and that it is independent of NYT.

Paul Krugman,

Your term 'asymmetry of fiscal risks', meaning that :

it's easier> to manage interest rates

than> to approve fiscal rescue,

maybe reworded to 'economic policy asymmetry',

is realist, important and deserves to enter Macroeconomics textbooks.

Congrats!